Earnings Lies & Why Munger Says “EBITDA Is Bull S**t”

Authored by Lance Roberts via RealInvestmentAdvice.com,

Earnings Worse Than You Think

Just like the hit series “House Of Cards,” Wall Street earnings season has become rife with manipulation, deceit and obfuscation that could rival the dark corners of Washington, D.C.

What is most fascinating is that so many individuals invest hard earned capital based on these manipulated numbers. The failure to understand the “quality” of earnings, rather than the “quantity,” has always led to disappointing outcomes at some point in the future.

As Drew Bernstein recently penned for CFO.com:

“Non-GAAP financials are not audited and are most often disclosed through earnings press releases and investor presentations, rather than in the company’s annual report filed with the Securities and Exchange Commission.

Once upon a time, non-GAAP financials were used to isolate the impact of significant one-time events like a major restructuring or sizable acquisition. In recent years, they have become increasingly prevalent and prominent, used by both the shiniest new-economy IPO companies and the old-economy stalwarts.”

Back in the 80’s and early 90’s companies used to report GAAP earnings in their quarterly releases. If an investor dug through the report they would find “adjusted” and “proforma” earnings buried in the back.

Today, it is GAAP earnings which are buried in the back hoping investors will miss the ugly truth.

These “adjusted or Pro-forma earnings” exclude items that a company deems “special, one-time or extraordinary.” The problem is that these “special, one-time” items appear “every” quarter leaving investors with a muddier picture of what companies are really making.

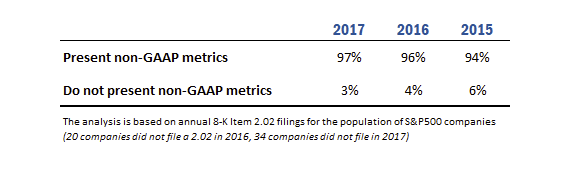

An in-depth study by Audit Analytics revealed that 97% of companies in the S&P 500 used non-GAAP financials in 2017, up from 59% in 1996, while the average number of different non-GAAP metrics used per filing rose from 2.35 to 7.45 over two decades.

This growing divergence between the earnings calculated according to accepted accounting principles, and the “earnings” touted in press releases and analyst research reports, has put investors at a disadvantage of understanding exactly what they are paying for.

As BofAML stated:

“We are increasingly concerned with the number of companies (non-commodity) reporting earnings on an adjusted basis versus those that are stressing GAAP accounting, and find the divergence a consequence of less earnings power.

Consider that when US GDP growth was averaging 3% (the 5 quarters September 2013 through September 2014) on average 80% of US HY companies reported earnings on an adjusted basis. Since September 2014, however, with US GDP averaging just 1.9%, over 87% of companies have reported on an adjusted basis. Perhaps even more telling, between the end of 2010 and 2013, the percentage of companies reporting adjusted EBITDA was relatively constant, and since 2013, the number has been on a steady rise.

So, why do companies regularly report these Non-GAAP earnings? Drew has the answer:

“When management is asked why they resort to non-GAAP reporting, the most common response is that these measures are requested by the analysts and are commonly used in earnings models employed to value the company. Indeed, sell-side analysts and funds with a long position in the stock may have incentives to encourage a more favorable alternative presentation of earnings results.”

If non-GAAP reporting is used as a supplemental means to help investors identify underlying trends in the business, one might reasonably expect that both favorable and unfavorable events would be “adjusted” in equal measure.

However, research presented by the American Accounting Association suggests that companies engage in “asymmetric” non-GAAP exclusions of mostly unfavorable items as a tool to “beat” analyst earnings estimates.

How The Beat Earnings & Get Paid For It

Why has there been such a rise is Non-GAAP reporting?

Money, of course.

“A recent study from MIT has found that when companies make large positive adjustments to non-GAAP earnings, their CEOs make 23 percent more than their expected annual compensation would be if GAAP numbers were used. This is despite such firms having weak contemporaneous and future operating performance relative to other firms.” – Financial Executives International.

The researchers at MIT combed through the annual earnings press releases of S&P 500 firms for fiscal years 2010 through 2015 and recorded GAAP net income and non-GAAP net income when the firms disclosed it. About 67 percent of the firms in the sample disclose non-GAAP net income.

The researchers then obtained CEO compensation, accounting, and return data for the sample firms and found that “firms making the largest positive non-GAAP adjustments… exhibit the worst GAAP performance.”

The CEOs of these firms, meanwhile, earned about 23 percent more than would be predicted using a compensation model; in terms of raw dollars. In other words, they made about $2.7 million more than the approximately $12 million of an average CEO.

It should not be surprising that anytime you compensate individuals based on some level of performance, they are going to figure out ways to improve performance, legal or not. Examples run rampant through sports from Barry Bonds to Lance Armstrong, as well as in business from Enron to WorldCom.

This was detailed in a WSJ article:

“One out of five [20%] U.S. finance chiefs have been scrambling to fiddle with their companies’ earnings.”

This rather “open secret” of companies manipulating bottom line earnings by utilizing “cookie-jar” reserves, heavy use of accruals, and other accounting instruments to flatter earnings is not new.

“The tricks are well-known: A difficult quarter can be made easier by releasing reserves set aside for a rainy day or recognizing revenues before sales are made, while a good quarter is often the time to hide a big ‘restructuring charge’ that would otherwise stand out like a sore thumb.

What is more surprising though is CFOs’ belief that these practices leave a significant mark on companies’ reported profits and losses. When asked about the magnitude of the earnings misrepresentation, the study’s respondents said it was around 10% of earnings per share.“

Manipulating earnings may work in the short-term, eventually, cost cutting, wage suppression, earnings adjustments, share-buybacks, etc. reach an effective limit. When that limit is reached, companies can no longer hide the weakness in their actual operating revenues.

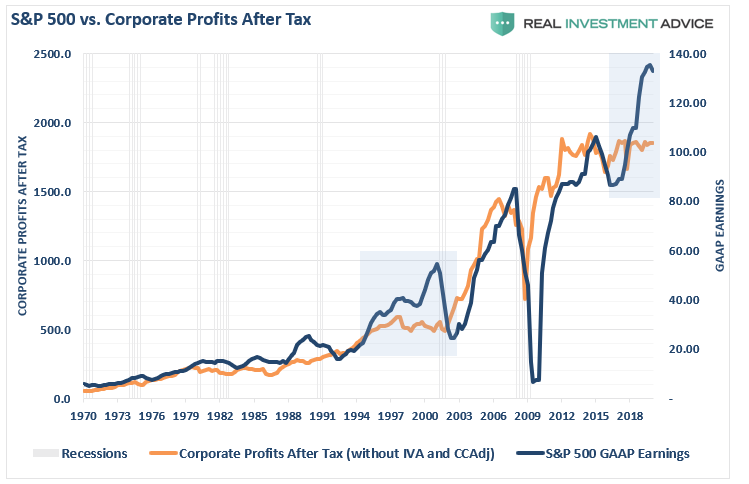

There’s a big difference between companies’ advertised performance, and how they actually did. We discussed this recently by looking at the growing deviation between corporate earnings and corporate profits. There has only been one other point where earnings, and stock market prices, were surging while corporate profits were flat. Shortly thereafter, we found out the “truth” about WorldCom, Enron, and Global Crossing.

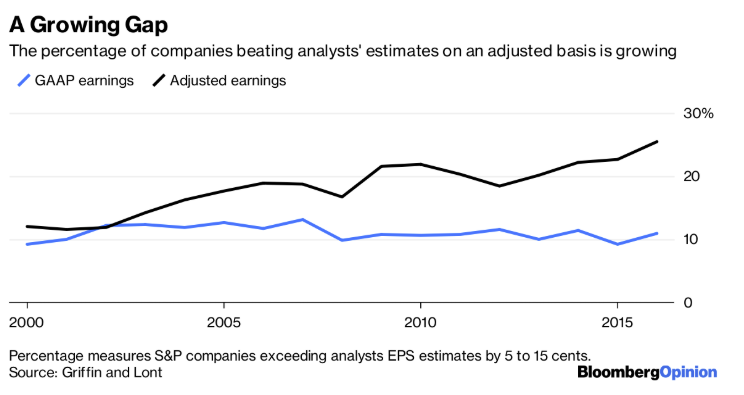

The American Accounting Association found that over the past decade or so, more companies have shifted to emphasizing adjusted earnings. But those same companies’ results under generally accepted accounting principles, or GAAP, often only match or slightly exceed analysts’ predictions.

“There are those who might claim that so far this century the U.S. economy has experienced such an unusual period of economic growth that it has taken analysts and investors by surprise each quarter … for almost two decades. This view strains credulity.” – Paul Griffin, University of California & David Lont, University of Otago

After reviewing hundreds of thousands of quarterly earnings forecasts and reports of 4,700 companies over 17 years, Griffin and Lont believe companies shoot well above analysts’ targets because consistently beating earnings per share by only a penny or two became a red flag.

“If they pull out all the accounting tricks to get their earnings much higher than expected, then they are less likely to be accused of manipulation.”

The truth is that stocks go up when companies beat their numbers, and analysts are generally biased toward wanting the stock they cover to go up. As we discussed in “Chasing The Market”, it behooves analysts to consistently lower their estimates so companies can beat them, and adjusted earnings are making it easier for them to do it.

For investors, the impact from these distortions will only be realized during the next bear market. For now, there is little help for investors as the Securities and Exchange Commission has blessed the use of adjusted results as long as companies disclose how they are calculated. The disclosures are minimal, and are easy to get around when it comes to forecasts. Worse, adjusted earnings are used to determine executive bonuses and whether companies are meeting their loan covenants. No wonder CEO pay, and leverage, just goes up.

Conclusion & Why EBITDA Is BullS***

Wall Street is an insider system where legally manipulating earnings to create the best possible outcome, and increase executive compensation has run amok,. The adults in the room, a.k.a. the Securities & Exchange Commission, have “left the children in charge,” but will most assuredly leap into action to pass new regulations to rectify reckless misbehavior AFTER the next crash.

For fundamental investors, the manipulation of earnings not only skews valuation analysis, but specifically impacts any analysis involving earnings such as P/E’s, EV/EBITDA, PEG, etc.

Ramy Elitzur, via The Account Art Of War, expounded on the problems of using EBITDA.

“One of the things that I thought that I knew well was the importance of income-based metrics such as EBITDA, and that cash flow information is not as important. It turned out that common garden variety metrics, such as EBITDA, could be hazardous to your health.”

The article is worth reading and chocked full of good information, however, here are the four-crucial points:

-

EBITDA is not a good surrogate for cash flow analysis because it assumes that all revenues are collected immediately and all expenses are paid immediately, leading to a false sense of liquidity.

-

Superficial common garden-variety accounting ratios will fail to detect signs of liquidity problems.

-

Direct cash flow statements provide a much deeper insight than the indirect cash flow statements as to what happened in operating cash flows. Note that the vast majority (well over 90%) of public companies use the indirect format.

-

EBITDA, just like net income is very sensitive to accounting manipulations.

The last point is the most critical. As Charlie Munger recently stated:

“I think there are lots of troubles coming. There’s too much wretched excess.

I don’t like when investment bankers talk about EBITDA, which I call bulls— earnings.

It’s ridiculous. EBITDA does not accurately reflect how much money a company makes, unlike traditional earnings. Think of the basic intellectual dishonesty that comes when you start talking about adjusted EBITDA. You’re almost announcing you’re a flake.”

In a world of adjusted earnings, where every company is way above average, every quarter, investors quickly lose sight of what matters most in investing.

“This unfortunate cycle will only be broken when the end-users of financial reporting — institutional investors, analysts, lenders, and the media — agree that we are on the verge of systemic failure in financial reporting. In the history of financial markets, such moments of mental clarity most often occur following the loss of vast sums of capital.” – American Accounting Association

Imaginary worlds are nice, it’s just impossible to live there.

Tyler Durden

Mon, 02/24/2020 – 13:00