Dual Coronavirus, Oil Shocks Crash World Markets, 10Y Yield Craters, Futures Pinned Limit Down

Global stocks plunged with the Emini locked limit down for the longest period on record, crude oil tumbled as much as 33% as WTI plunged as low as $27.34, and the yield on the 10Y Treasury crashed to an all time low of 0.31% after Saudi Arabia launched a price war with Russia, sending investors already panicked by the coronavirus fleeing for safe assets.

As noted overnight, the catalyst for today’s historic rout was the plunge in crude, which tumbled as a result of Saudi Arabia launching an all out price war, one which may result in as much as a 4 million barrel production surplus per day, and which at one point tumbled more than 30%, the most since the Gulf War in 1991. After paring some losses, WTI and Brent remained down about 20%.

There were also worries that U.S. oil producers that had issued a lot of debt would be made uneconomic by the price drop.

As Bloomberg notes, the oil-price crash, if sustained, would upend politics and budgets around the world, exacerbate strains in high-yield credit and add pressure on central bankers trying to avert a recession. It typically would have proved a boon to consumers, but the coronavirus is increasingly keeping them at home.

Spooked by the implications for energy stocks, and the imminent crash in the junk bond market, S&P 500 futures fell 5%, triggering trading curbs designed to limit the most dramatic moves while cash markets are closed. Two major exchange-traded funds that track U.S. benchmark gauges posted even bigger declines in pre-market trading. They are not subject to the same curbs.

Predictably, US oil majors and oil services and equipment stocks plunged in pre-market trading, with shares of Chevron crashing 12% and Exxon Mobil dropping 10%. Services and equipment stocks also slumped, with Transocean -20%, Halliburton -16% and Schlumberger -15%. Numerous other companies in the energy sector, including Devon Energy, Occidental Petroleum and Marathon Oil fell at least 20%. In Europe, the Stoxx 600 Oil & Gas index fell as much as 15%, the most on record.

And since the limit-down move is likely to resume once stocks reopen, here are the threshold triggers for marketwide halts on the cash S&P500:

- If the S&P 500 declines 7%, (208 points), trading will pause for 15 min

- If declines 13%, (386 pts) trading will again pause for 15 mins

- If falls 20%, (594 pts) the markets would close for the day.

European stocks as measured by the Stoxx Europe 600 Index, fell the most since 2016 entering bear market territory and suffering hefty losses in early trade with London dropping more than 8%, Frankfurt falling more than 7% and Paris almost matching those losses. Several of the region’s gauges look set to enter bear markets and most of Italy’s stocks failed to open after the government ordered a lockdown of large parts of the north of the country, including the financial capital Milan.

Japanese stocks entered a bear market earlier when they tumbled almost 6%: in the Asian session, stocks slumped led by energy and materials, after Monday’s crash in oil prices added to the grim backdrop of the virus outbreak. All markets in the region were down, with equity gauges in Japan, Australia, and Singapore, Thailand and Indonesia each dipping by more than 7%. Shares in Japan, the Philippines, Singapore and Indonesia have plunged more than 20% from their highs as American stock-index futures slumped. The Lehman-like panic after Monday’s crash in oil prices adds to selling triggered by the virus outbreak that has infected almost 110,000 people worldwide and killed more than 3,800.

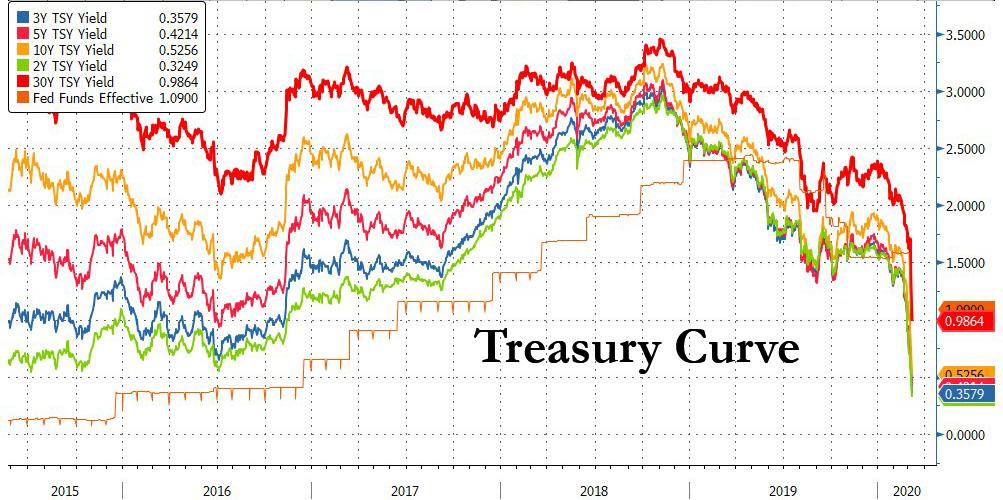

With traders unable to S&P futures – traditionally the most liquid equity-linked security in the market- they bought bonds instead, and the 10-year Treasury yield fell as low as 0.31%, the lowest ever…

… taking the whole U.S. yield curve below 1% for the first time in history.

In Europe, the spread between Italy’s 10-year sovereign yield and Germany’s jumped 33 basis points to 211 basis points, the highest since August as traders doubted the credibility of the ECB’s ability to preserve stability “whatever it takes.”

The turmoil hit FX as well, with exchange rates moving sharply as traders struggled to establish where new trading ranges might be. The yen was up about 3% versus the dollar, as the USDJPY briefly dipped below 102 in what appeared to be an overnight flash crash…

… while the euro and Swiss franc both rising more than 1%.

In case anyone missed the big news over the weekend, Saudi Arabia stunned markets with plans to raise its production significantly after the collapse of OPEC’s supply cut agreement with Russia, a grab for market share reminiscent of a drive in 2014 that sent prices down by about two thirds. The shock in oil was seismic, with Brent crude futures sliding $12 to $33.20 a barrel in chaotic trade.

Meanwhile the coronavirus pandemic continued to rage, with the number of people infected with the coronavirus topping 110,000 across the world as the outbreak reached more countries and caused more economic carnage.

Not helping the mood was news North Korea had fired three projectiles off its eastern coast on Monday.

“Wild is an understatement,” said Chris Brankin, Chief Executive at stockbroker TD Ameritrade Singapore. “Not just us, but across the globe you would have every broker/dealer raising their margin requirements … trying to basically protect our clients from trying to leverage too much risk or guess where the bottom is.”

“After a week when the stockpiling of bonds, credit protection and toilet paper became a thing, let’s hope we start to see some more clarity on the reaction,” said Martin Whetton, head of bond & rates strategy at CBA. “Dollar bloc central banks cut policy rates by 125 basis points, not as a way to stop a viral pandemic, but to stem a fear pandemic,” he added, while noting that many central banks had little scope to ease further.

A tectonic shift saw markets fully price in an easing of 75 basis points from the Fed on March 18, while a cut to near zero was now seen as likely by April. The ECB meets on Thursday and will be under intense pressure to act, but rates there are already deeply negative. Indeed, urgent action is clearly needed, with data suggesting the global economy toppled into recession this quarter. Figures out from China over the weekend showed exports fell 17.2% in January-February from a year earlier.

Finally, while commodities cratered, Gold initially cleared $1,700 per ounce to a fresh seven-year peak, only to fall back to $1,676.55 amid talk some investors were having to sell to raise cash to cover margin calls in stocks.

Thor Industries, Casey’s and Stitch Fix are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 4.9% to 2,819.00

- STOXX Europe 600 down 6.5% to 342.84

- MXAP down 4.2% to 149.95

- MXAPJ down 5% to 488.43

- Nikkei down 5.1% to 19,698.76

- Topix down 5.6% to 1,388.97

- Hang Seng Index down 4.2% to 25,040.46

- Shanghai Composite down 3% to 2,943.29

- Sensex down 5.9% to 35,352.82

- Australia S&P/ASX 200 down 7.3% to 5,760.56

- Kospi down 4.2% to 1,954.77

- German 10Y yield fell 12.1 bps to -0.831%

- Euro up 1.3% to $1.1429

- Italian 10Y yield rose 0.5 bps to 0.906%

- Spanish 10Y yield rose 6.8 bps to 0.282%

- Brent Futures down 20% to $36.18/bbl

- Gold spot up 0.4% to $1,667.55

- U.S. Dollar Index down 0.6% to 95.34

Top Overnight News from Bloomberg

- The Federal Reserve is under intensifying pressure to tackle the increasing risk of a worldwide credit crunch as falling commodity prices combine with the spreading virus to hammer financial markets

- Panic reigned in currency markets as orders from traders and algorithmic machines snowballed to spur some of the biggest moves since the global financial crisis

- Euro Stoxx 50 futures dropped more than 4% early on Monday amid mounting worries over the spread of the coronavirus in Europe and after Italy announced drastic measures including a near-complete travel ban for about a quarter of Italians as the number of cases in the country soared

- Oil markets crashed more than 30% after the disintegration of the OPEC+ alliance triggered an all-out price war between Saudi Arabia and Russia that is likely to have sweeping political and economic consequences

- The Trump administration is drafting measures to blunt the economic fallout from coronavirus and help slow its spread in the U.S., including a temporary expansion of paid sick leave and possible help for companies facing disruption from the outbreak, according to three people familiar with the matter

- The coronavirus has spread to about half of the world’s countries, with global fatalities reaching 3,800 and infections in Italy eclipsing those in South Korea. Italy introduced far-reaching measures to contain the outbreak, though it remained unclear how strictly they would be enforced. The U.S. is asking Americans to avoid cruise ships as it prepares to move more than 3,000 passengers and crew off the Grand Princess vessel

- Gold rallied above $1,700 an ounce as a concerted global rush into havens intensified, with the upswing driven by turmoil in the oil market, the spread of the coronavirus, sinking equities, and expectations of easier monetary policy as recession risks loom ever larger

- Japan’s economy contracted last quarter more than initially estimated, underscoring its vulnerability even before the coronavirus threatened to push the country into recession.

- Boris Johnson will announce a 5 billion pound ($6.5 billion) investment in the U.K.’s next generation broadband internet services as he seeks to ensure that remote parts of the country can benefit

- The euro-area economy may be headed for its first recession in seven years as the coronavirus outbreak takes an increasing toll on businesses and consumer confidence. Economists at Morgan Stanley and Berenberg expect the euro-zone gross domestic product to shrink in the first half of the year. In France, the central bank now sees output barely growing in the first quarter

- “A temporary decline in activity in some sectors is in fact preferable to a prolonged crisis that would risk expanding to all sectors of the economy,” Italy’s Finance Ministry says in statement Monday on the government’s drastic virus containment measures

- German January industrial production rose 3% from the previous month, compared with an estimate for a 1.7% increase

Asian equity markets resumed their slump and US equity futures also suffered heavy losses in which the E-mini S&P hit limit down and DJIA futures pointed to another decline of over-1000 points, as oil prices slipped by around 30% after Saudi Arabia kicked off an oil price war. The kingdom announced plans to raise its output to over 10mln bpd beginning next month and it cut the OSP for all destinations by USD 6-8/bbl following last week’s breakdown of the OPEC+ output deal in which Russia rejected the proposal for additional cuts. ASX 200 (-7.3%) posted its largest intraday loss in more than 11 years amid a collapse across the energy sector although gold miners bucked the trend due to the flight to safety, while Nikkei 225 (-5.1%) gapped below 20K and continued to tumble against the backdrop of the detrimental currency flows and following the miss on Q4 GDP which further pointed to the likelihood of a looming recession. Hang Seng (-4.2%) and Shanghai Comp. (-3.0%) conformed to the sell off as blue-chip energy names were pummelled and after continued PBoC liquidity inaction, while the latest trade data from China over the weekend showed a surprise Trade Deficit and a larger than expected contraction in Exports. Finally, 10yr JGBs were higher amid the bloodbath in stocks and as it tracked the advances in T-notes which surged nearly 2 points as US 10yr and 30yr yields delved into unprecedented levels, while the BoJ were also present in the market today for nearly JPY 1tln of JGBs.

Top Asian News

- Japan GDP Shrinks More Than Estimated, Fueling Recession Concern

- Debt-Default Showdown Looms as Lebanon Freezes Bond Payment

- Global Rout Threatens to End China’s Leverage-Loving Stock Binge

- Saudi Prince Tests Grip on Power With Desert Raid, Oil Price War

European opened substantially into negative territory this morning (Stoxx 50 -6.6%) as sentiment remains subdued on the coronavirus, but with the added development of a crude-war between Saudi Arabia and Russia after the OPEC+ bust-up on Friday (Full details available in the commodity section below). It’s worth noting that sentiment has begun to recuperate somewhat, with US equity futures trading briefly above the limit down positions that were hit overnight (Limit Down Details). Given the commitments from Saudi to increase production to over 10.0mln BPD as of next month and they have cut the official selling price for all destinations by around USD 7/bbl, crude prices are as such lower by over USD 10/bbl and the energy sector has similarly recoiled (Stoxx Oil & Gas -13%). The Oil & Gas Sector accounts for 5.5% of the Stoxx 500 itself, and the largest weightings withing the sector are Total at 29.4%, BP with 15.5% and Shell contributing 14.5%; in terms of price performance, they are currently down by 13.3%, 15.7% and 16.7% respectively. Additionally, the overall downside is exacerbated by the FTQ seen overnight which has sent the global yield complex to record lows for most core parties. For instance, the entirety of the US yield curve is below 1% for the first time and the German 10yr low thus far resides at -0.86%. The Stoxx banking sector is the sector with the 3rd largest weighting in the Stoxx 600 representing 9.4% and is currently 7.3% down on the day. Elsewhere, sectors are all firmly in the red as is every open component in the Stoxx 600 itself; note, a number of Co’s failed, at least initially, to open. Looking ahead, focus turns to how markets react to the US’ entrance, particularly whether this exacerbates the sell-off; as well as for any indicative signs from any particular Co’s in the Energy/Banking sector regarding profit warnings, guidance changes or other telling comments

Top European News

- Italy Bond Yields Soar as Virus Lockdown Hits Financial Capital

- Germany Boosts Investment to Protect Economy From Virus Hit

- Putin Dumps MBS to Start a War on America’s Shale Oil Industry

- France Economy Hit by Virus as Central Bank Slashes Outlook

In FX, risk sentiment has been roiled by Saudi Arabia’s decision to increase output and slash the cost of crude in response to the breakdown of OPEC+ talks last week when Russia refused to back a deeper cut in production, as prices tumble and compound fears over the economic fallout from China’s nCoV. Eur/Nok has hit highs just shy of 11.0000 and Eur/Sek topped 10.7500, while Usd/Rub peered over 75.0000 before WTI and Brent nursed some losses from just above Usd27 and Usd31 per barrel respectively. Meanwhile, Usd/Cad catapulted to 1.3750+ at one stage overnight and the Antipodean Dollars saw flash crashes that dragged Aud/Usd and Nzd/Usd down to circa 0.6320 and 0.6030, but the Loonie, Aussie and Kiwi have all clawed back some lost ground as their US peer succumbs to pressure from sliding Treasury yields and more pronounced bull-flattening along the curve, not to mention heavy depreciation vs safer havens.

- JPY/EUR/CHF/GBP – In stark contrast to all the above, Usd/Jpy has been trading largely in lock-step with oil with added impetus from risk-off flows/positioning between wide 104.58-101.58 parameters and the Yen retains a strong underlying bid unlike GOLD that has faded from a few bucks over Usd1700/oz at best on profit taking and long liquidation. Elsewhere, Eur/Usd hit resistance just ahead of 1.1500 and Usd/Chf based a few pips under 0.9200 as Eur/Chf bottomed around 1.0510 in advance of Swiss jobs data and sight deposits showing another rise in bank balances. Similarly, Cable waned after touching 1.3200 with Sterling still subject to hard Brexit jitters alongside the coronavirus and crude capitulation that pose growth and financial stability threats. However, the DXY remains vulnerable itself within a 95.694-94.719 range and not far from a key technical level at worst (94.080 representing a 50% retracement from ytd peak).

- EM – Severe underperformance in extreme or bordering on unprecedented levels of aversion, especially through the cross-over from Asia-Pacific to European time zones has ravaged regional currencies, though the Lira has rebounded more than most on the vastly cheaper oil price as a net importer and the Yuan is holding firmly above 7.0000 after another decline in the Usd/Cny fix.

In commodities, a frantic session for commodities to say the least after sources over the weekend noted that Saudi Arabia will be boosting its output to above 10mln BPD from this month’s 9.7mln BPD as a response to the collapse of its OPEC+ alliance with Russia. Saudi is also said to have told market participants that it could raise output to as much as 12mln BPD, although sources stated that the initial increase is likely to total between 10-11mln BPD in April, with the final figure contingent on refiners’ response to price cuts. Furthermore, the Kingdom slashed its official pricing for crude, with oil giant Aramco cutting its Asia prices for Arab Light crude and Medium crude by USD 6/bbl each, to discounts of USD 3.10/bbl and USD 4.05/bbl below the Middle East benchmark respectively. In a challenge to Russia, the company made the largest cut to northwest Europe of some USD 8/bbl in most grades – Russia sells a bulk of its Urals crude in the same region. Arab Light sales to Europe will be at a USD 10.25/bbl discount to Brent – levels not seen since at least May 2002. As a result of the anticipated rising production and slash in OSPs – expected to flood the market with barrels – WTI and Brent futures sank 27% and 30% respectively, with the former paused for a few minutes following its aggressive >7% move. WTI Apr’20 briefly slipped below USD 28/bbl vs. Friday’s USD 41.50/bbl close, while Brent May 20 dipping south of USD 32/bbl vs. Friday’s USD 45.50/close – with the spread also narrowing to ~USD 3.80/bbl vs. ~4/bbl on Friday. The Kingdom hopes the slump in oil prices and the expected diminishing in Russia’s market shares will prompt Moscow back to the negotiating table and force its hand to cut output. Desks note that although this may prove effective in the short-term, it is in less certain what the longer-term impact will be. The front-month energy contracts have, as European players entered the markets, pared some losses with WTI Apr’20 now back to ~USD 32.50/bbl, with the 29th Jan 2016 low at USD 26.19/bbl, whilst the Brent May contract reclaimed a USD 36/bbl status. Away from the OPEC debacle, IEA cut 2020 world oil demand forecasts by almost 1mln BPD, due to the coronavirus; envisage the first contraction since 2009, noting that Demand could drop by 730k BPD, in an extreme event where Gov’t fails to contain the virus. Price action to the report was muted given the omission of a scenario that incorporates the weekend Saudi/Russian news. Elsewhere, spot gold failed to hold onto impetus from the global stock rout after prices briefly surpassed USD 1700/oz to the upside to prices last seen in December 2012. The yellow metal then waned off highs and into negative territory – potentially on profit-taking and as investors pump money into government debts in search of safe-haven assets. Meanwhile, copper conformed to the overall risk tone and gapped lower at the open, losing the USD 2.5/lb handle to a current low of USD 2.4675/lb.

US Event Calendar

- Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

When you’ve worked through the Asian crisis, the Russian/LTCM crisis, the 2000 equity bubble collapsing, the GFC, the European sovereign crisis, and several other smaller wobbles it takes a lot to stun you in financial markets. However the weekend news-flow and overnight price action in oil – just at a time a beaten up market could have done without it – has done that and deserves its own place in the history books.

Following the 10% plunge in oil prices on Friday, WTI and Brent are down a further -30.01% and -27.55% this morning respectively to $28.80/bbl and $32.73/bbl and more or less at their lows since Asia opened. For context this is the largest absolute one-day decline for Brent crude ever while in % terms the decline is the highest since January 17, 1991 when it dropped by -34.8% during the gulf war. This follows the developments over the weekend, specifically that Saudi Arabia plans to raise oil production next month through targeting market share rather than supply management, therefore leading to the threat of an all-out price war following a breakdown in OPEC talks. This led to huge declines in Middle Eastern markets yesterday with bourses in Abu Dhabi, Dubai, Saudi Arabia and Kuwait down between 5% and 10%. The main Kuwait index actually suspended trading in the biggest shares after falling 10% while Saudi Aramco fell below its IPO price for the first time. DB’s Michael Hsueh published a note yesterday suggesting that oil should migrate below $20 now. See here for his full analysis. Our economists have often attributed the collapse in inflation expectations in 2015-16 to the collapse in oil prices. They haven’t really recovered from this and are likely to take a further dent now. With central banks running out of road the good news is that this should put us closer to more fiscal spending and likely helicopter money. That might not be the first reaction today though.

The plunge in oil has led to complete capitulation in other markets this morning. In rates, 10y and 30y Treasuries have traded below 0.50% and 1.00% respectively (currently 0.513% and 0.968% as we go to print – moves of -24.6bps and -31.9bps since Friday) meaning the entire yield curve has is below 1% for the first time in history. In equity markets losses are being led by the Nikkei (-5.82%) with further big legs lower for the Hang Seng (-3.50%), Shanghai Comp (-2.14%) and Kospi (-4.14%). It’s worth noting that Australia’s ASX index – typically a perceived defensive market in Asia Pacific – is even down -7.33%. S&P 500 futures are down -5% and have hit circuit breakers. Meanwhile 10y JGBs traded down -0.20% although have since nudged slightly higher, Gold is flat, other base metals are down heavily (iron ore down over 4%), while the Yen (+2.73%) and Swiss Franc (+1.48%) have rallied at the expense of oil sensitive currencies.

One area that will be under severe scrutiny given the oil move is credit. Energy makes up 14% of overall US HY whereas for context in the S&P 500 the energy sector is more like 3% of the overall index. The timing of this is very bad as fears were building in credit already on Friday. As a proxy and showing the demand for hedges, EU Crossover had one of its worst days since the GFC – widening c.60bps. I always think that if a management consultant firm was asked to look at the credit market and report back on its functioning I think they would say that it’s disingenuous to call it a market. The reality is that if you want to buy large amounts at new issue you can do so. However if you wanted to sell it back weeks, months or years later you would only be able to generally do it in much smaller sizes. Dealers only have small appetite to absorb risk even in good times. This massive imbalance doesn’t matter when you have a decent economy and constant inflows as you’ve had for most of the last decade. However once investors have doubts about the economy and/or see outflows then selling can overwhelm the market. The danger of the current situation is you’re starting to risk seeing the early stages of such a move. If this crisis is prolonged it’s likely that credit will see big liquidity air pockets that will spook other asset classes and risk becoming a viscous circle. Its possible central banks will intervene but probably only after bigger problems first. This is part of the reason we extended our spread widening view last Thursday (see link here ) although we now have a tighter spread target for YE than we did at the start of the year. Staying with credit Craig and Nick on Friday put out a note looking at US profit warnings seen so far and also those companies they see at being at risk of downgrades, including those at risk of being junked. See their report here.

Overnight, the Australian newspaper reported that the Australian government will announce a fiscal stimulus package of AUD 10bn while the SKY news was reporting that the plan would likely include cash handouts. So more and more countries are pivoting towards the idea of helicopter money. The US is also drafting measures to blunt the economic fallout from coronavirus and help slow its spread in the US, including a temporary expansion of paid sick leave and possible help for companies facing disruption from the outbreak (per Bloomberg) as New York became 2nd state to declare a state of emergency after cases in the state reached 106. Further, the G20 also made a similar statement to that of G7 over the weekend saying they would use “fiscal and monetary measures, as appropriate, to aid in the response to the virus, support the economy during this phase and maintain the resilience of the financial system.”

Meanwhile, the latest on the virus is that Italy is now close to becoming the worst affected country after China with 7,375 confirmed cases and 366 deaths. Italian PM Giuseppe Conte announced quarantine measures affecting 16mn people yesterday as anyone living in Lombardy and 14 other central and northern provinces will need special permission to travel with Milan and Venice both affected. Schools, gyms, museums, nightclubs and other venues will remain close across the whole country and the moves are likely to remain in place till April 3rd. In other news, Bloomberg is reporting that the Trump administration has told their Chinese counterparts that the purchasing boost, signed in January as part of the Phase 1 trade deal, with specific target dates and commodities, could start off slowly due to the virus hit. However, the US has indicated that this is only an option as long as there isn’t a jump in Chinese exports when virus-related industrial shutdowns end. Elsewhere, the Institute of International Finance highlighted in a report the EM capital outflows hit $30bn in 45days due to the coronavirus outbreak. The amount exceeds the outflows observed during the 2015 China devaluation scare and the 2007-2008 global financial crisis.

It’ll feel like an age ago now, but last week markets saw one of the most volatile weeks in nearly a decade, with the intraday and closing moves on the S&P 500 at sizes unseen since the US debt downgrade in 2011. Prior to this morning the 10-year U.S. Treasury yield was half of what it was 2 weeks prior on 22-Feb having fallen over -70bps to end the week at 0.762% (-15bps Friday, -39bps last week), and saw an all-time intraday low of 0.66% Friday morning almost exactly 11 years after the GFC lows of 666 on the S&P 500. The S&P 500 posted its 10th decline in 12 sessions on Friday (-1.71% but off the -4.05% lows for the session), but actually ended the week slightly higher +0.61%, after two days of over 4% rallies midweek. Since its record high on Feb. 19, the index is down over 12% and has lost $3.43 trillion of market capitalization. The main lagging sectors on the week were banks and energy stocks again as rates and oil both sunk. 30y US treasuries fell to an all-time low of 1.287% – down -38.8bps on the week (-25.3bps Friday). While oil fell to nearly 3 year lows as virus related growth scares and the inability for OPEC+ to get Russia to agree to production cuts – Brent was down -9.44% on Friday (-10.39% on the week) – that is the commodity’s largest one day loss since March 8th 2000, almost 20 years to the day.

It was a similar story in Europe as the STOXX 600 fell -2.36% on the week (-3.67% on Friday) underperforming the US partly as it was closed when risk markets had a late NY rally on Friday. As the virus outbreak spreads through Italy, the government has now indicated they are going to implement €7.5 billion of fiscal stimulus, as the FTSE MIB was down -1.79% on the week (-3.62% Friday). 10yr bund yields are back flirting with late summer 2019 all-time lows and now at -0.71%, falling -2.4bps on Friday and -10.3 bps over the week, while spreads in France, Italy, and Spain were all 3.5-7.5bps wider over the course of the week. Credit spreads were wider as well on both HY and IG – US HY was 58bps wider on the week (59bps Friday), while IG was 19bps wider on the week (14bps Friday). In Europe, HY was 36bps wider on the week (36bps Friday), while IG was 12bps wider on the week (9bps Friday). The VIX has now closed over 30 for a full week for the first time since October 2011. Lastly, gold finished the week at its highest levels since Feb 2013 as the prospects of central bank easing and an economic slowdown increase, the haven was up over +5.5% on the week.

As for this week, the focal point will be the ECB meeting on Thursday. Following the Fed’s emergency rate cut this week our economists believe that this has made it easier for the ECB to disappoint market expectations and inadvertently tighten financial conditions; and Christine Lagarde’s hope to shift more of the burden of policy stimulus to fiscal policy will be tested. Our team’s expectation for policy is twofold. The first element is unconditional. Our colleagues expect the ECB to announce a targeted and temporary liquidity facility to support SME lending in affected regions. This ‘quantity of financing’ policy can be complemented by ensuring sufficient eligible collateral and flexibility within NPL rules. The second element is conditional; a 10bp deposit rate cut in April, signalled in March. This cut is conditioned on the virus spreading further and the tightening of financial conditions spreading sufficiently beyond equities into bank funding costs, sovereign funding costs and/or EUR exchange rate appreciation.

In the UK there will be some focus on the government’s 2020 budget, due to be unveiled by Chancellor of the Exchequer Rishi Sunak on Wednesday. In the US further democratic primaries are scheduled, with the bulk coming on Tuesday with 6 states reporting including Idaho, Michigan, Mississippi, Missouri, North Dakota and Washington. In terms of data it’s going to still be pretty backward looking so rather than go through if we’ll leave you to read the day-by-day calendar below.

Tyler Durden

Mon, 03/09/2020 – 07:51