Putin Front-Runs QE, Proposes Taxing Investment Outflows

Authored by Tom Luongo via Gold, Goats, ‘n Guns,

Russia is going to be a destination for safe-haven flows in the post-COVID-19 world. It will be due to its vast savings, prudent fiscal policy and maneuver room available in monetary policy.

The biggest reason, however, for why I think Russia looks attractive to foreign investors is simply because of its political stability. Putin deftly proposed to devolve power out of the presidency and reorganize both his cabinet and the current government before the outbreak.

And while the final vote on these changes has been delayed because of COVID-19 they will very likely pass without incident when the worst of the crisis in Russia is over.

The same cannot be said for Russia’s neighbors in Europe, where the response has been both heavy-handed and inadequate to stem the tide against the virus.

And given the extreme fragility of the European banking system the response on the financial side both fiscally and through monetary policy will destroy what little confidence exists there.

When no less than former ECB President Mario Draghi is writing in the Financial Times to justify dropping the fiduciary equivalent of a nuclear bomb on Europe, you know things are desperate.

You only bring out the big guns when things are ready for substantive change.

Read Draghi’s words carefully and you’ll notice the only time he references the past is to justify, what else, war spending. There is no other way to fight this fight.

We must print all the money in the world and destroy the futures of our grand children in order to save ourselves today. It’s typical apocalyptic rhetoric from someone who was the architect of the current system’s fragility in the first place.

Draghi actively destroyed not only real capital and real wealth with negative interest rates he destroyed the sovereign debt market in Europe by buying up whole swaths of it.

Christine Lagarde came in this morning to continue Draghi’s work, pushing down European bond yields after the U.S. Senate approved the biggest stimulus package in our history.

And into this mess Russia will also be spending money. Most of this was money already earmarked for this year. Putin is no Austro-libertarian or anything. There’s going to be stimulus in Russia.

And that’s why, at the same time, he’s looking to shore up Russia’s tax reciepts by shifting some of the tax burden to those looking to take advantage of what are now very high real rates of return on Russian capital.

Putin is putting a 15% tax (or tariff) on dividends paid to foreign entities as a way to front run the influx of capital fleeing the destruction that’s happening around Russia.

I was contacted for a comment by Sputnik News on this and here’s what I had to say:

“Putin is trying to get in front of capital outflow in the case of a wider global recession since Russian companies are more likely to weather that storm better than in a lot of other countries”, the analyst says.

Luongo underscores that the Russian president has recently put an emphasis on the concept that companies which “benefitted from the state’s assistance should be held to account for bettering Russia”. Likewise, “international investors should be on the hook paying back that assistance”, he notes.

According to Luongo, the Kremlin is “also trying to ensure that Russia as a destination for capital fleeing the chaos in the West doesn’t become a kind of ‘high-yield’ slush fund”.

“Russia is about to spend a lot of money in support of its economy and Putin understands that as the West struggles Russia will be seen as an emerging safe haven”, he adds. “And this tariff on dividends is a way of attenuating that and offsetting lower oil tariffs”.

With oil at or below $30 per barrel there is now a much bigger hole in Russia’s budget as tariffs from domestic oil and gas producers will likely drop to near zero. Russian Finance Minister Anton Siluanov expects a shortfall of RUB 3 trillion next year (~$38.7 billion).

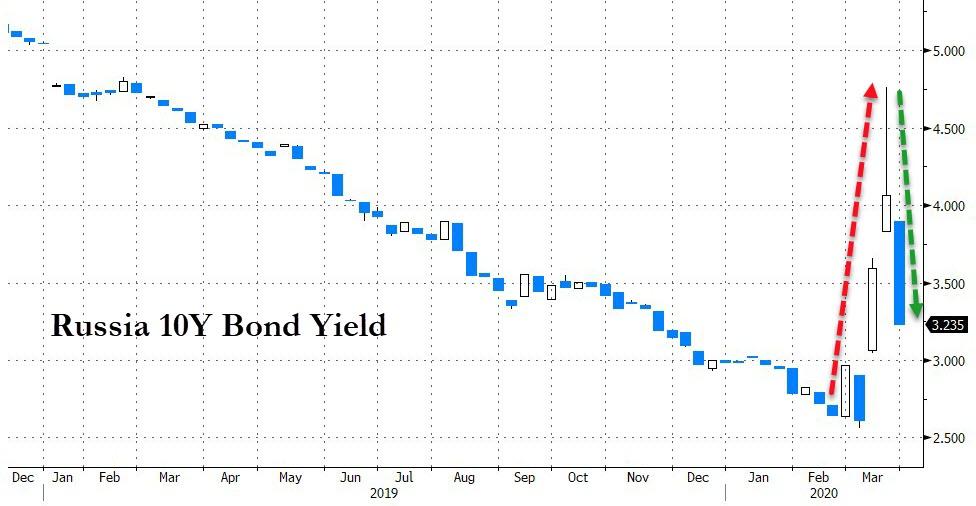

So, some of that money can be made up elsewhere and taxing foreign investors looking for easy 10-12% real yields makes sense. Currently Russian 10 year government bonds trade around 7%. That number is likely to continue falling back to its longer-term run rate since yield curves in the West are getting crushed right now thanks to QE and further financial repression.

When most western economies are going to be contracting between 5-10% for the next couple of quarters the potential real yields for investors is very tasty. And it makes sense for Putin to want to 1) slow that down and 2) offset the lost oil revenues.

Into this market the Bank of Russia could easily sell into demand and recoup a lot of its coupon payments on the back end through this tariff without having to lower rates to over-stimulate the Russian domestic markets.

But, these are all secondary effects. The main effect is to protect the domestic economy from capital inflow that does nothing to assist the development of Russia’s non-oil economy.

As all those new trillions in bailout money come in to blow a bubble in Russian assets and take all the money right back out again when a slightly better deal comes along.

I’m no fan of tariffs but in a world of unlimited money printing a move like this makes sense, especially now that you are public enemy #1 for having helped precipitate the crash overseas in the first place.

* * *

Join My Patreon because you hate QE. Install the Brave Browser if you want to help mitigate QE

Tyler Durden

Thu, 03/26/2020 – 20:45