Morgan Stanley’s Oracle Turns Bearish Again: “Stocks Are Now Overbought… A Correction Will Begin Soon”

For much of 2019, Morgan Stanley’s chief equity strategist Michael Wilson issued a weekly sermon of fire and brimstone in his Monday Morning market takes, which contrasted with the generally euphoric pronouncements by his peers at other banks – most notably Goldman, which in December hilariously declared that the US economy is “structurally less recession-prone today” (oops) earning him the moniker of Wall Street’s biggest bear (a few permabearish exceptions such as Albert Edwards were excluded from the tally), not to mention quite a few angry clients.

But then, in November, just as the melt up phase of the post “Not QE” market was kicking in sending stocks to all time highs every single day, Wilson got the proverbial tap on the shoulder and threw in the towel raising his S&P “bull case” price target to 3,250, however not without a slew of warnings that the most likely outcome was another retest in stocks lower.

In retrospect, Wilson should have held fast to his bearish conviction as the unprecedented March market crisis confirmed he was spot on (even if for different reasons).

Yet even then Wilson made it clear he had been on the fence, and was only forced into the bullish camp due to the the aggressive central bank intervention launched in late 2019. Little did he know what was coming, and that’s also why when most of his formerly uber-bullish colleagues were issuing one downgrade after another, Wilson threw all caution to the wind and officially became the biggest Wall Street bull shortly after the March 23 lows, when just a few days later he said that “we are buyers of dips” and recommending that – because most stocks have been in a bear market for two years or longer (most stocks except for the Top 5 that techs that matter) investors should “start buying stocks now because we cannot be sure if the next pull back will lead to lowers lows or not given we already experienced forced liquidation. Bottom line, we believe 2400-2600 on the S&P 500 will prove to be very good entry points for those with a time horizon of 6-12 months.“

This time Wilson timed his call almost perfectly, with the S&P surging since his bullish reversal, with his declaration that 2400-2600 in the S&P will be a market floor so far proving correct.

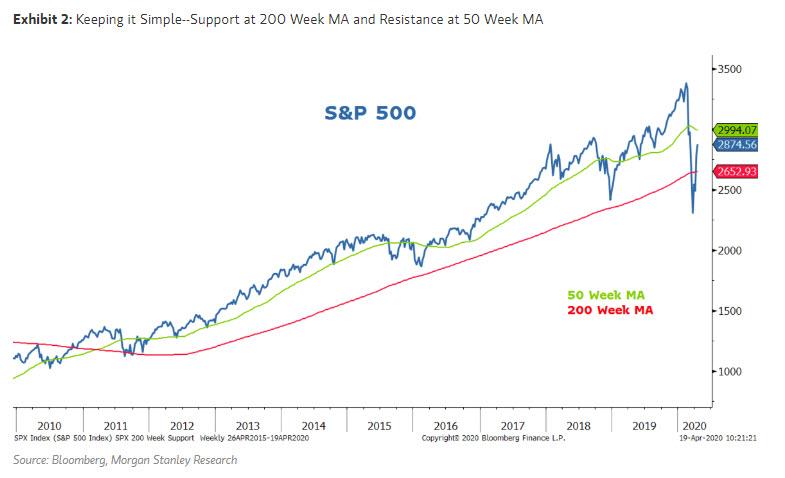

But with stocks having soared to just shy of 2,900 last week, is Wilson still bullish? According to his latest note, the answer is “not any more” and in fact he is now expecting a sharp pullback, to wit “with risk assets now overbought, the chance for a correction has increased.” In S&P 500 terms, Wilson sees stocks as continuing to trade in a range between 2,600 and 300, noting that the S&P “will find strong support at the 200 week moving average, or 2650″ and should markets continue to look through the near term bad news on earning, “it should face resistance at the 50 week moving average, or 2995.”

Here are some more details that justify Wilson’s latest U-turn:

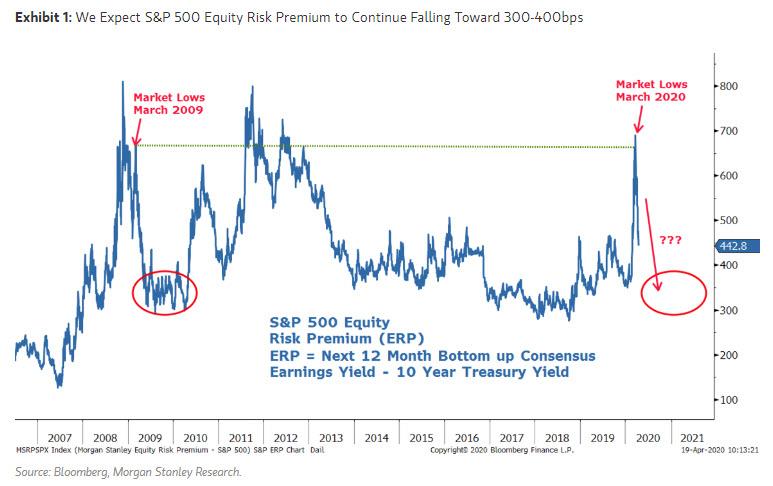

Our over arching view continues to be that the equity market bottomed in March on what amounted to a forced liquidation. The monetary policy response has been effective in stabilizing credit spreads and equity risk premiums which reached the same level observed at the lows of the Great Financial Crisis in March, 2009 (Exhibit 1). Therefore, it is unlikely we will approach such levels again any time soon. Meanwhile, fiscal programs appear to be getting the money to their desired destinations after a slow start which should support both consumers and small businesses until the economy can get reopened. In fact, the PPP program has already run out of money with increases now being debated in Washington.

And so, with many risk assets now overbought, Wilson says he would “not be surprised if a correction in US equities begins soon.” The reasons for this are that in addition to what is likely to be a partisan debate on more fiscal stimulus, the MS strategist expects more bad news from companies on earnings results as well as their outlooks for 2020.

As previously stated, the market is looking past this year as a write off and is trying to calculate what 2021 will look like, in some cases pricing earnings off of 2022 forecasts which, as we have said previously, will be dead wrong. Wilson agrees with our skepticism, saying that while 2021 will likely be better than 2020 (unless a depression has begun in which case it won’t “it’s also hard to have much precision or confidence about the magnitude of the snap back we should expect.”

Wilson also suspects that company guidance will portray similar uncertainty which could weigh on asset prices over the next few weeks. Furthermore, that uncertainty should weigh greatest on those stocks which are still under-discounting the magnitude of the declines in 2020. In short, ‘high expectation’ stocks are the most vulnerable to a near term correction. And, as noted above, Wilson expects the index to find very strong support at the 200 week moving average, or 2650. Likewise, should markets continue to look through the near term bad news, it should face resistance at the 50 week moving average, or 2995.

Tyler Durden

Tue, 04/21/2020 – 13:36