US Oil Rig Count Collapses As Wave Of Shale Well Closures Begins

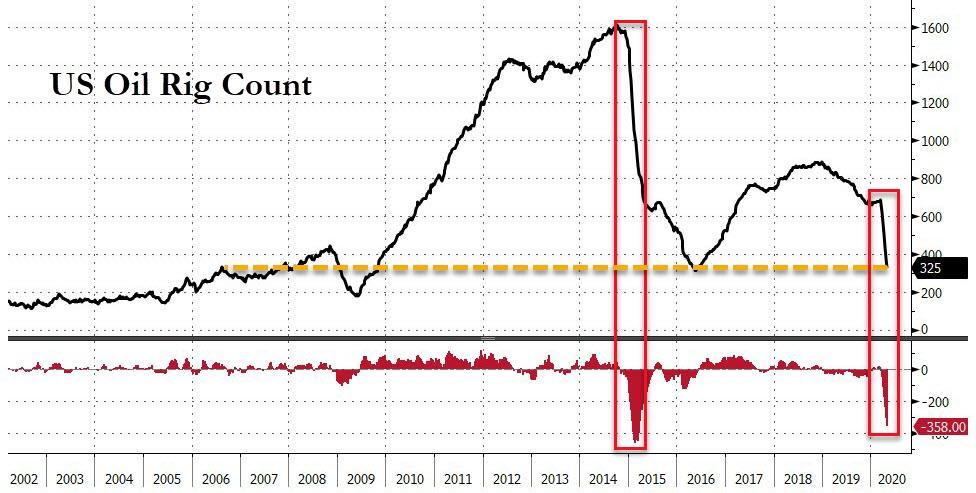

For the 7th straight week, the US oil rig count has plunged (down 53 to 325). This is the biggest drop since the 2015 collapse and the same total oil rig count first seen in 2006…

And while U.S. shale oil producers have so far held up admirably, hanging on for dear life amidst the biggest oil demand collapse in history. the rig count collapse may signal more trouble ahead as American producers continued to pump at record highs in March, even after dozens of drillers laid out blueprints to limit production.

But, as OilPrice.com’s Alex Kimani notes, with U.S. storage about to hit tank tops in a matter of weeks and the world deep in the throes of the biggest pandemic in modern history, the inevitable has begun to unfold: The arduous and costly process of well shut-ins.

Oil production in the country tumbled sharply to 12.2 million bpd in the third week of April, a good 900,000 bpd less than the record peak of 13.1 million bpd recorded just a month prior. That’s a 7% production cut in the space of only a few weeks and the lowest level since July.

A lot more could be on the way.

More Production Cuts

Oklahoma-based Continental Resources (NYSE:CLR), the company controlled by billionaire Harold Hamm, has ceased all its shale operations in North Dakota and shut in most wells in its Bakken oil field totaling roughly 200,000 bpd.

The company, though, has refused to sell its contracted oil to pipelines at negative prices by declaring force majeure.

Continental has defended its stance by pointing out that the coronavirus outbreak has “…brought about conditions under which force majeure applies” while adding that selling its oil at negative prices constitutes waste.

Continental made the risky gamble of betting that economic growth would lift prices and, therefore, left itself heavily exposed to low oil prices by failing to employ the industry’s usual playbook of hedging future production with derivatives.

Continental is in good company, though.

Rystad Energy via CNBC has reported that six major U.S. shale producers will shut another 300,000 bpd of crude in May and June. That’s ~100,000 bpd more than April cuts, thus bringing the country’s total production cuts to 1.2 million bpd. The cuts will come from Continental Resources, ConocoPhillips (NYSE:COP), Cimarex Energy (NYSE:XEC), Enerplus Corporation (NYSE:ERF), Parsley Energy (NYSE:PE) and PDC Energy (NYSE:PDCE).

Continental Resources is set to slash 69,000 bpd in April and nearly 150,000 in May and June while ConocoPhillips will lower output by 125,000 bpd of oil equivalent, including 60,000 bpd of oil.

Rystad’s head of shale research, Artem Abramov, has estimated that the biggest shale fields–Permian, Eagle Ford, and Bakken–will cut a further 900,000 bpd, 250,000 bpd, and 400,000 bpd, respectively, throughout 2Q20, with shut-ins accounting for a staggering 60% in the early stages.

Expensive Shut-Ins

A well shut-in is considered a drastic action of last resort mainly because it can result in huge or even total loss of production.

That’s a big consideration in these dire times, where even oilfield values are descending into negative territory due to liabilities such as plugging wells and land remediation.

Chris Atherton, president of EnergyNet, a company that deals in oil and gas operations, undeveloped acreage and royalty interests, has told Forbes that oilfield prices have tumbled from an average price of $42,000 per net flowing barrel per day when oil prices were around $60/barrel to under $20,000 currently. Buyers started getting picky and sellers more desperate in 2019 when oil prices were still relatively high.

Things have gone to the dogs now, with a shut-in field fetching only half the price of a virtually identical field but with oil still flowing.

As Bob Bracket of Bernstein Research revealed last week, “Shut-ins are not easy decisions. When production shuts-in, problems arise. Multi-phase well flows begin to separate out, while problematic hydrates, waxes, asphaltenes form which will have serious economic implications,” citing numerous examples of fairly large wells with flows exceeding 1,000 barrels/day that could not be brought back to life after being shut-in.

That’s the main reason why even heavily indebted shale companies, including bankrupt ones like Whiting Corp. (NYSE:WLL), insist on continuing to pump at all costs.

California Resources Corp. (NYSE:CRC) is a $133.7M (market cap) company drowning in debt to the tune of more than $4 billion due by the end of 2022. The company’s average all-in cost per barrel of $35 means that it’s losing ~$20 for each barrel of crude it pumps. Yet, the company is unable to shut-in its wells because they require a continuous injection of steam to keep them alive.

Deal Mania

A shut-in well is a tough proposition for a prospective oilfield buyer, too, because it’s hard to determine how much oil can be coaxed out, especially after a lengthy layoff.

The only solace for the beleaguered oil sector is that there probably won’t be a shortage of takers when the worst is finally over.

Atherton says that his company has 40,000 registered users with access to $17 billion in cash ready to make deals. He has predicted that distressed companies will “turn into a flood of assets available” in a year or so.

The bottom hunters will certainly be waiting to pounce, the downside being that many investments in the space could turn worthless due to the swelling wave of bankruptcy.

Tyler Durden

Fri, 05/01/2020 – 13:11