If The Bear Market Is Over, Why Are Commodities & Transports Underperforming?

Authored by Bryce Coward via Knowledge Leaders Capital blog,

As Steve highlighted yesterday, we are beginning to see some important divergences develop between the stock market and other data that suggest we are not out of the woods yet.

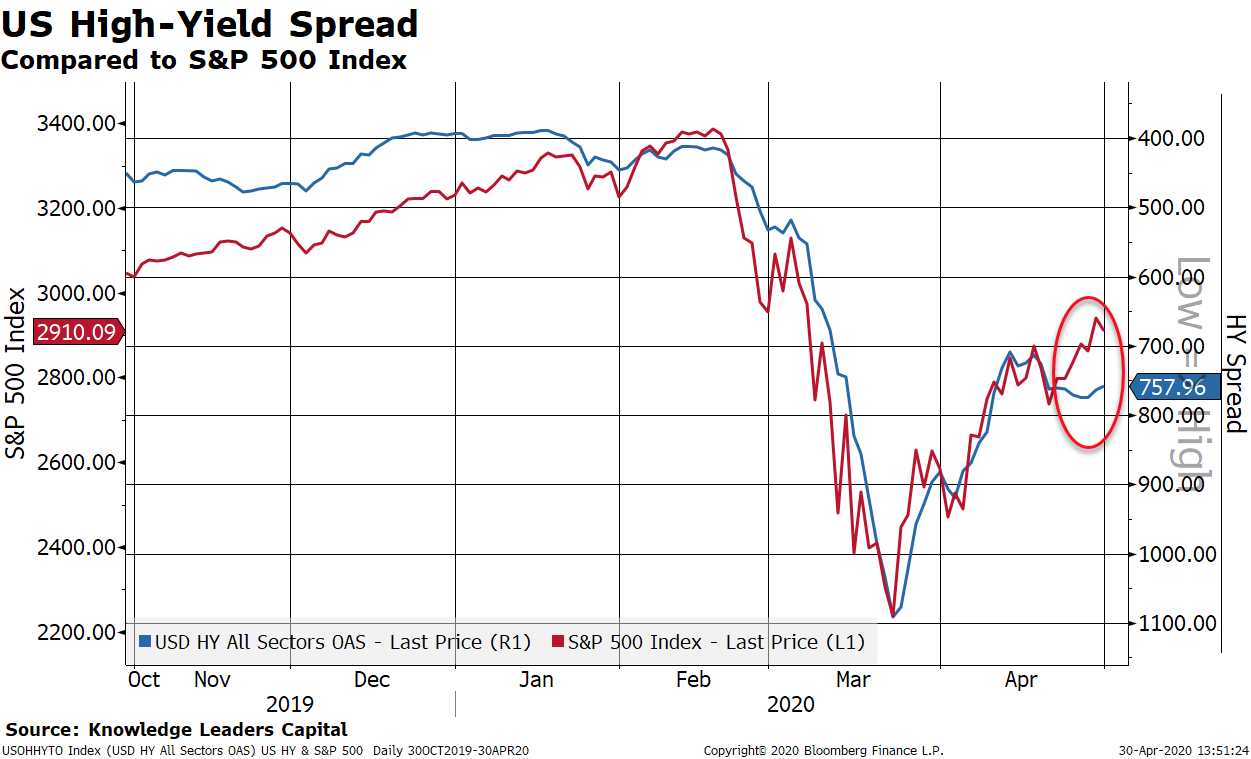

…the divergence between high yield spreads and the S&P 500 suggests the possibility of a roughly 5% correction in stocks.

Unless of course one believes that HY spreads continue to contract. With economic growth falling off a cliff, the later may be the less plausible scenario.

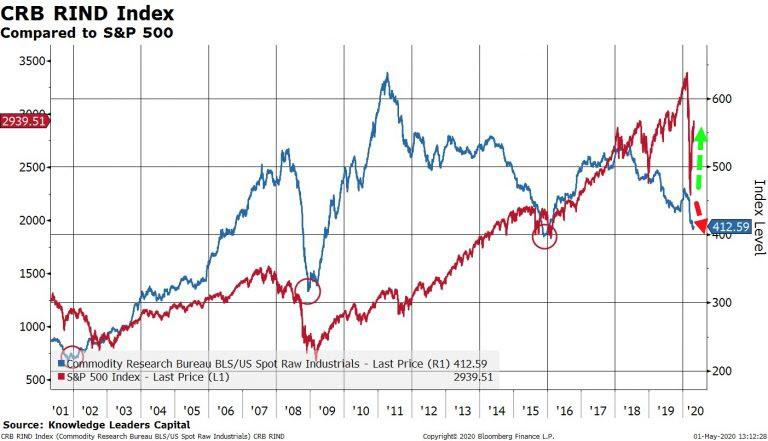

Of course, this makes complete sense since next week we may learn of an unemployment rate with a 20-handle. Recovering from this destruction is unlikely to be quick or easy or without setbacks. Certainly, that is the message from two of the most cyclical indicators we track, commodity prices and transport stocks.

As this first chart shows, industrial commodities have typically bottomed in price well before stocks have bottomed during bear markets. This was the case in 2001, 2008 and 2015. Currently, commodity prices as measured by the CRB Raw Industrial Commodity Index are at cycle lows. This is an unsettling divergence that tells us that demand for raw materials is still falling, a condition not typically seen in front of an economic rebound.

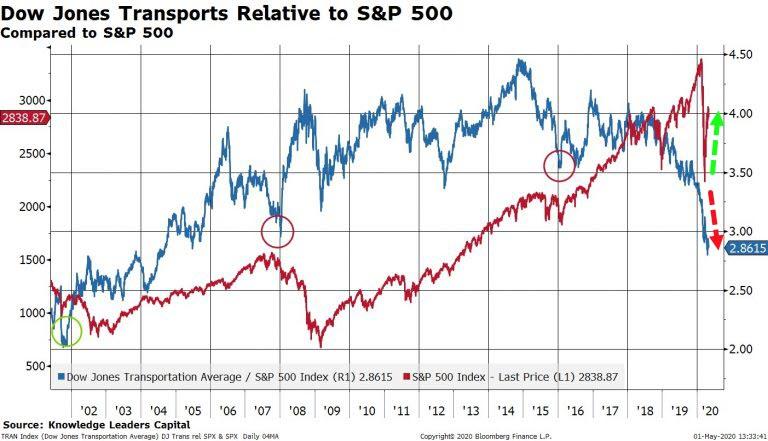

Similarly, transport stocks are healthily underperforming the broad stock market index. Transports bottomed before the overall stock market in 2001, 2008 and 2015 so new relative performance lows is concerning.

Of course, airlines are particularly impacted by COVID shutdowns, but the transport stocks should still anticipate a bottoming of economic activity by outperforming the broad market.

Their failure to do so is of concern.

Tyler Durden

Sun, 05/03/2020 – 10:40