US To Borrow A Record $4.4 Trillion In 2020, More Than The Previous Five Years Combined

So much can change in three months.

Back on February 3, the Treasury in its quarterly announcement of marketable borrowing estimates was delighted to announce that “During the April – June 2020 quarter, Treasury expects to pay down $56 billion in privately-held net marketable debt, assuming an end-of-June cash balance of $400 billion.”

Well, oops.

Fast forward to today, when one global (still ongoing) coronavirus pandemic, and one global economic crisis later, the Treasury now expects to boost the net amount of marketable Treasury debt outstanding by an unprecedented $3 trillion in the April-to-June quarter in order to fund the trillions in stimulus and bailout payments.

This is what the Treasury said about its latest borrowing needs:

During the April – June 2020 quarter, Treasury expects to borrow $2,999 billion in privately-held net marketable debt, assuming an end-of-June cash balance of $800 billion. The borrowing estimate is $3,055 billion higher than announced in February 2020.

According to the Treasury, the surge in borrowing needs is “driven by the impact of the COVID-19 outbreak, including expenditures from new legislation to assist individuals and businesses, changes to tax receipts including the deferral of individual and business taxes from April – June until July, and an increase in the assumed end-of-June Treasury cash balance.”

But wait there’s more because looking at the next quarter (July though September) the Treasury now expects to borrow an additional $677 billion in privately-held net marketable debt, assuming an end-of-September cash balance of $800 billion.

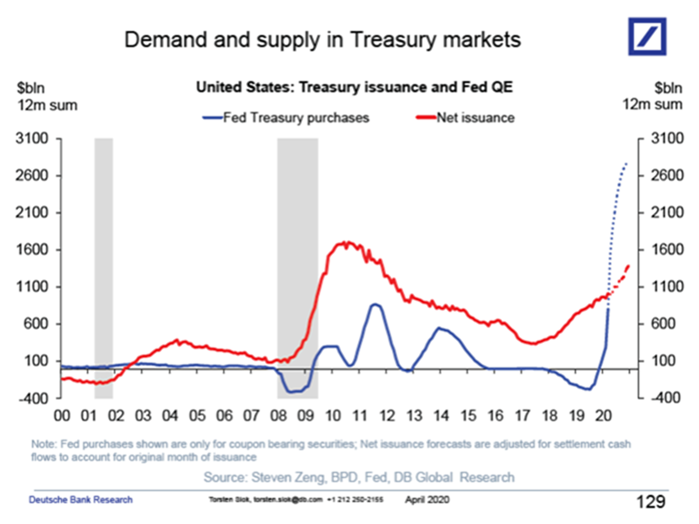

In other words, the Treasury will borrow a record $3.7 trillion in the 6 month interval from April to September. This also explains why the Fed – which has already purchased $2.5 trillion in securities in the past 6 weeks – is currently monetizing double the total Treasury net issuance: because it is preparing for precisely this eventuality.

Finally, in the first calendar quarter of the year, quarter, the Treasury borrowed $477 billion in debt – $110 billion more than it had originally expected – ending the quarter with a cash balance of $515 billion

This is summarized in the table below.

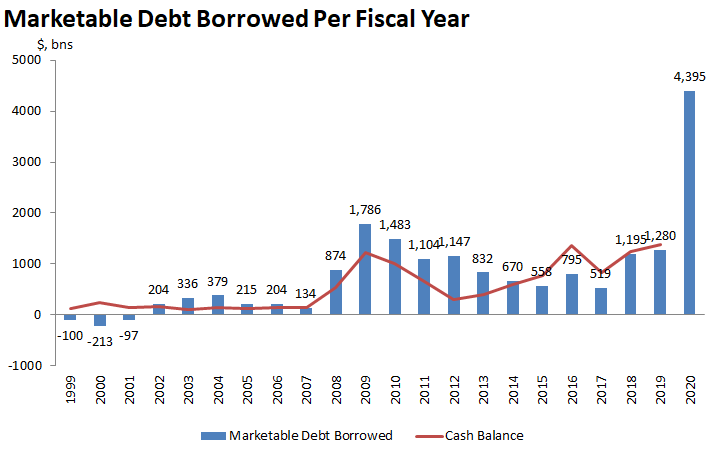

Summarizing this data, Reuters’ Jeoff Hall writes that US marketable debt borrowing in FY’20 is on track to reach $4.395 tn, up from $1.280 tn in FY’19 or $1.195 tn in FY’18. It is more than the previous five fiscal years combined and almost 2.5x the previous record high borrowing for any fiscal year (FY’09$1.786 tn).

Commenting on the revised borrowing estimates before they were released, Jefferies analysts Thomas Simons and Aneta Markowska said that “The world has changed quite a lot” since the Treasury’s last estimates three months ago, noting – correctly – that the revisions this quarter would be “profound and historic.”

They sure were, and since the bulk of this new issuance will come in the form of T-Bills as Treasury gradually ramps up its coupon auctions, the question is whether – as Zoltan Pozsar warned recently – the Fed may lose control over Bill yields, which so far are holding in but should the market start worrying about the coming surge in issuance, that may not be the case for much longer.

In a note discussing the potential complications from this “Billnado” as it called it, Deutsche Bank warned that “in recent history bill supply has been disruptive to short-dated funding generally as bills absorbed cash that might have otherwise been invested in other assets such as repo or CP. This is of course a potential outcome in the current case as well.”

How to avoid a potential front-end crisis? Here is what Pozsar suggested several weeks back:

The Fed has done a lot and yield curve control where they peg three month Treasury bill yields at OIS rates and is the only thing the Fed has not done yet, but soon will have to. The target range for overnight rates and the OIS curve – the bottom layer of the money market cake – are the Fed’s monetary sanctum. Everything the Fed does is priced based on variables within that sanctum: the top of the band, IOR, IOR plus a spread and OIS plus a spread.

Deutsche Bank agreed:

With inflation stuck below target and likely to move lower, inflation expectations anchored at uncomfortably low levels, and unemployment rising sharply, the Fed has every reason to ensure that financial conditions remain exceptionally accommodative. In this context, we foresee the Fed adopting front-end yield curve control (YCC) in late Q2 or Q3 that sets caps on Treasury yields out to about three years.

As such, Today’s Teeasury announcement starts the clock on a Fed announcement where the Fed will unveil Yield Curve Control stretching from T-Bills all the way to ultra long dated coupons, which for now mean 30Y but in the future could include 100Y bonds as well as perpetuals…

Tyler Durden

Mon, 05/04/2020 – 16:30