It Begins: For The First Time Ever, Futures Price “Fatal” Negative US Rates Starting Jan 2021

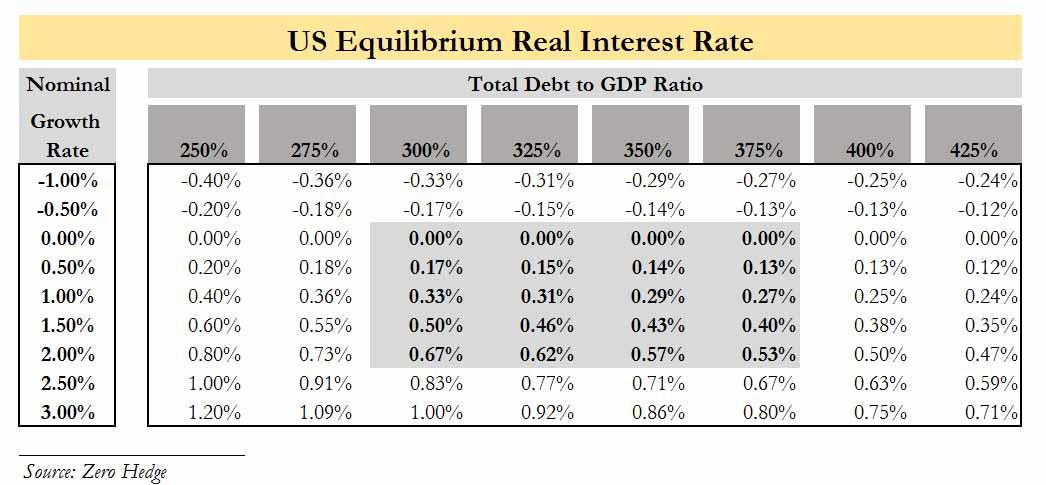

Back in 2015, when the Fed set off on its first tightening cycle in a decade and was set to hike rates for the next three years, we wrote in an article that in retrospect would be proven 100% correct, in which we warned that by hiking rates the Fed is engaging in a massive policy error, because according to our calculations at the time, r* (r-star), or the natural rate of interest in an economy where total debt/GDP was 350% and rising, and where GDP was 2% and falling, the short-run equilibrium real interest rate was a paltry 0.57%…

… which also meant that any attempts to push rates notably higher – as the Fed was doing then – would result in catastrophe (recall the Ghost of 1937 when the Fed engaged in an identical policy error), forcing the Fed to promptly cut rates, if not go negative. This is precisely what the Fed figured out three years later, in late 2018 when it gave up on any hopes of interest rate normalization and proceeded to cut rates again.

Fast forward to today, when the US debt is far greater, while GDP growth is, well nobody really knows but as of this moment is imploding and deeply negative. Logically, that would mean that r* is far, far lower than it was back in 2015. And just last week, Deutsche Bank confirmed as much, when its credit strategists concluded that despite the massive intervention by the Fed to date, it will need to do more to catch down to r*.

As DB’s Stuart Sparks wrote on April 26, “there is ample evidence that policy must ease further in a variety of asset markets. One of these is the currency market. The trade weighted dollar is stronger than it was before the Covid-19 shock, and is stronger than it was when effective funds were more than 225 bp higher last year. Another clear reflection of further need for policy easing is in commodity markets. Oil has nearly monopolized commodityrelated headlines, but are only part of the story: agricultural commodities and metals are significantly lower on the year. We can see this in breakevens, where our model fair value is roughly 1% and clearly no where near the context of Fed policy objectives.“

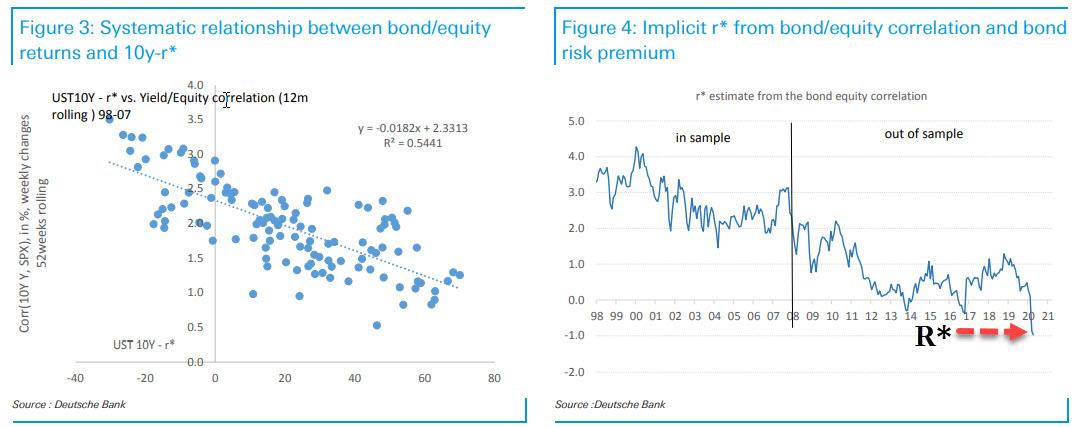

As Sparks further explain, if indeed policy is not easy enough, precisely how easy should it be? What is the optimal level of real short rates, or r*? While market dynamics can suggest that policy remains too tight, r* is not directly observable in real time. We frame this discussion with an estimate of r* developed by our colleague Francis Yared in a recent piece in which he presents evidence from equity/fixed income correlations that suggests r*is approximately -1%.

As the DB strategist then concludes, “given observable correlations and Treasury yields, we can infer the level of r* implicit in market behavior.“

The conclusion is scary: despite everything the Fed has done – which includes trillions in explicit liquidity injections and implicit funding backstops – not only does the Fed need to do more, but it would in fact have to cut rates to negative to offset pent up market imbalances.

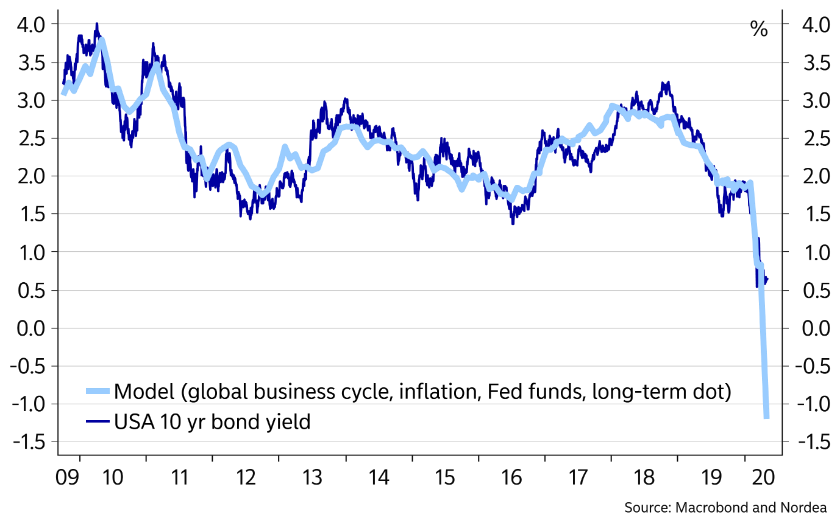

Deutsche Bank wasn’t alone in its dire assessment: in a report published today Nordea’s FX strategist Andreas Steno Larsen went even further than the German Bank, writing that according to the bank’s model, “negative long USD yields could be the name of the game” and references the following chart correlating 10Y Treasurys with its implied yield which uses inputs from the global business cycle, inflation, Fed Funds, and the Fed’s long-term dot.

Of course, earlier this week we got Ken Rogoff writing a Project Syndicate piece earlier this week, “The Case for Deeply Negative Interest Rates” in which he wrote “imagine that, rather than shoring up markets solely via guarantees, the Fed could push most short-term interest rates across the economy to near or below zero. Europe and Japan already have tiptoed into negative rate territory. Suppose central banks pushed back against today’s flight into government debt by going further, cutting short-term policy rates to, say, -3% or lower.“

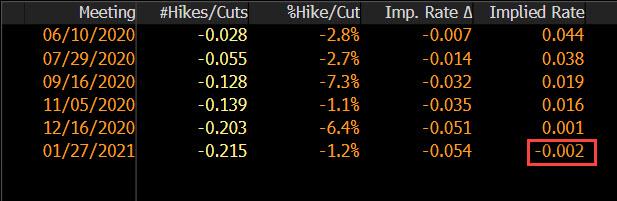

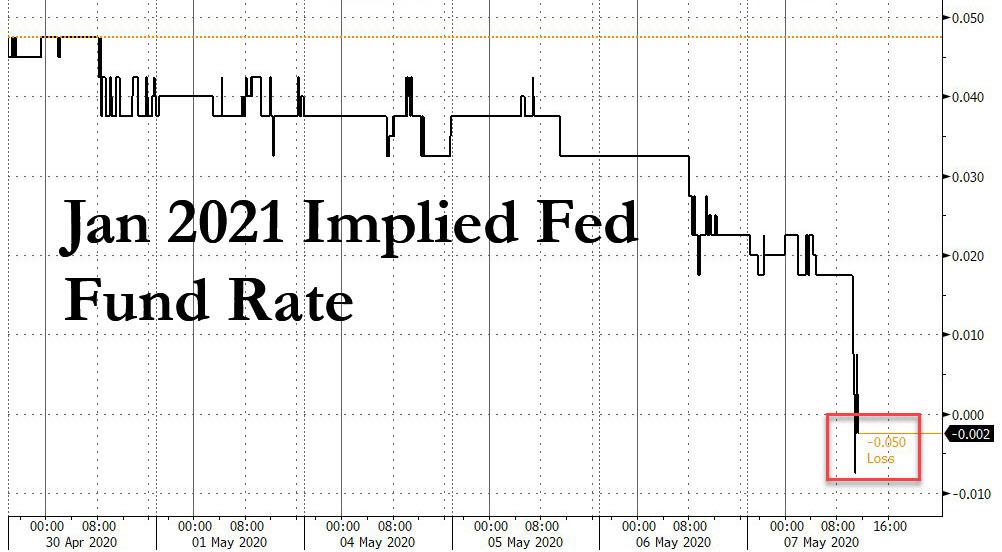

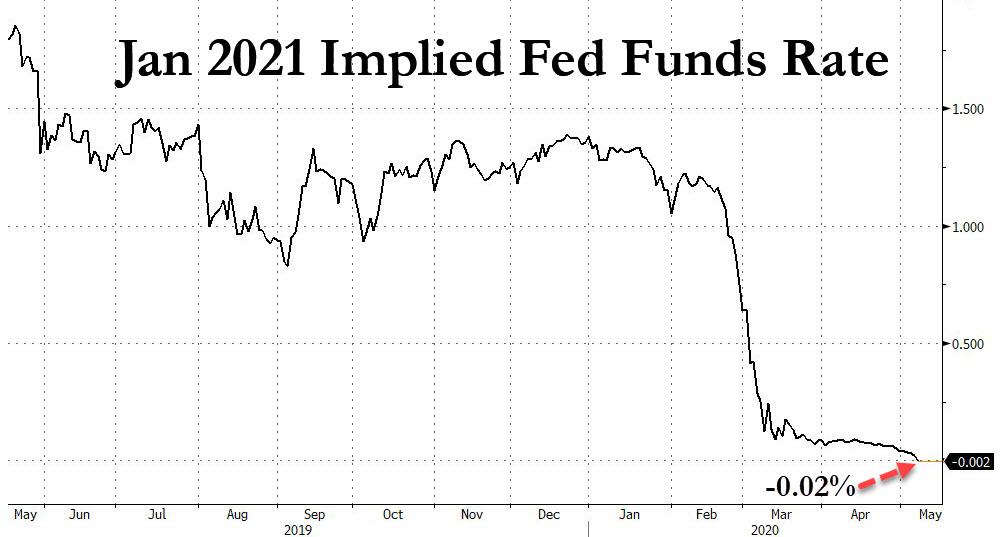

Facing this barrage of negative rate commentary and forecasts, the market appears to have finally relented and moments ago the Bloomberg WIRP function showed something that has never happened before: the January 2021 implied rate is now a negative -0.02%…

… the first time this series has dipped into the negative!

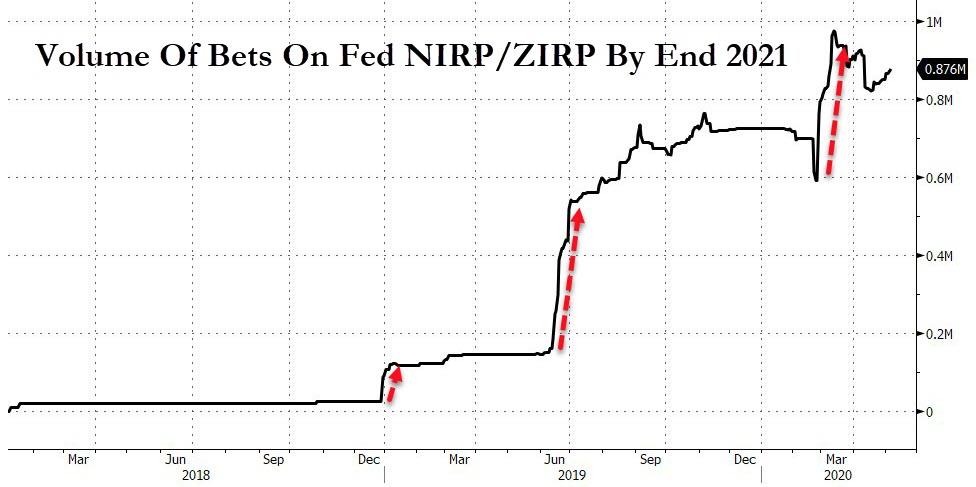

Understandably, the volume of bets on NIRP by end of 2021 has been surging, and sure enough the market finally cracked in what is the most serious test of the Fed’s conviction to not impose negative rates.

What does a negative interest rate mean, aside from the obvious death sentence for banks? We have written thousands of articles (literally) why sliding into this monetary twilight zone – where both Japan and Europe already are to be found, frozen in monetary carbonite – means game over, but instead of recapping them all, we will give the final word to the bond king Jeff Gundlach himself, who conveniently summarized it best last night when he tweeted that a rate < 0 is "fatal".

These Trillions Treasury is borrowing is heavily in T-Bills. Chair Powell has stated in plain English he is opposed to negative interest rates. Yet the pressure to go negative on Fed Funds will build as short term borrowing explodes and dominates. Please, no. Rates < 0 = Fatal.

— Jeffrey Gundlach (@TruthGundlach) May 6, 2020

Tyler Durden

Thu, 05/07/2020 – 11:31