“Clueless Wizards” – Don’t Worry, The Fed Has “Belts & Suspenders”

Tyler Durden

Tue, 05/26/2020 – 12:25

Authored by Mike Shedlock via MishTalk,

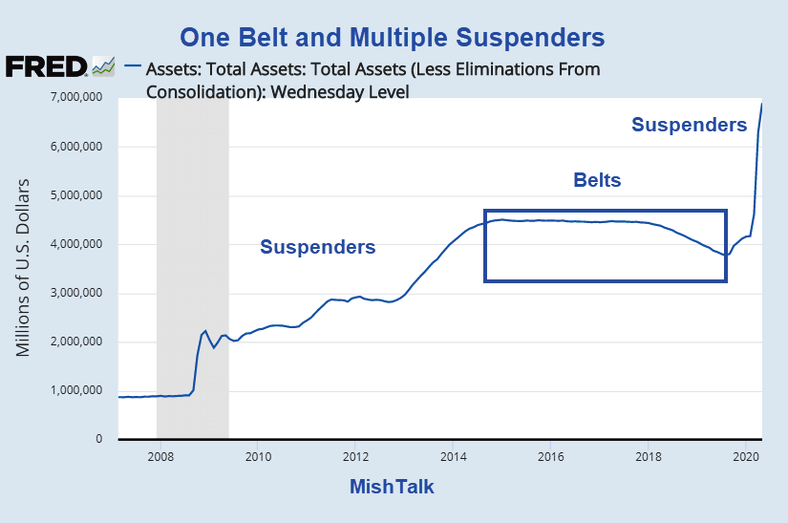

The Fed’s balance sheet is approaching $7 trillion dollars. This is what Bernanke meant by suspenders.

On February 27, 2013, Ben Bernanke spoke to US Congress about how the Fed would unwind its balance sheet.

Bernanke said, We Have “Belts, Suspenders” to Unwind Balance Sheet .

Bernanke’s vague answer to Sen. Richard Shelby, R-AL, when asked how the Fed will deleverage the balance sheet, was this: “In terms of exiting from our balance sheet… a couple of years ago we put out a plan; we have a set of tools. I think we have belts, suspenders – two pairs of suspenders. I think we have the technical means to unwind at the appropriate time; of course picking the exact moment to do, of course, is always difficult.”

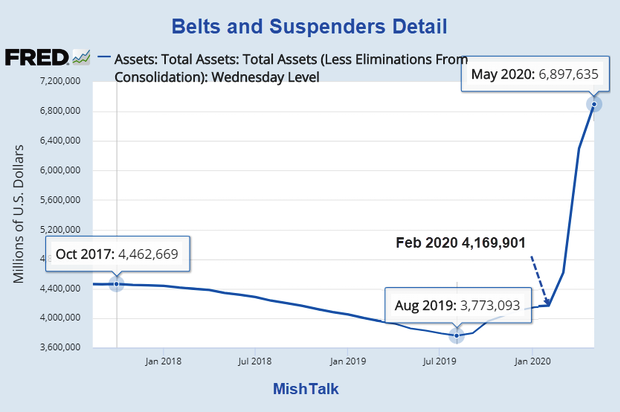

Belts and Suspenders Detail

Belts and Suspenders Synopsis

-

Belt tightening took the Fed’s balance sheet from $4.46 trillion to $3.77 trillion.

-

Suspenders took the Fed’s balance sheet from $3.77 trillion to $6.90 Trillion in just 9 months.

Tapering, That’s All You Get

Please recall the September 18, 2019 QE Debate: What Did Powell Mean by “Need to Resume Balance Sheet Growth”?

Powell’s Prophecy

“And we are going to be assessing the question when it will be appropriate to resume the organic growth of our balance sheet.”

More prophetic words have seldom been heard.

Some objected to my post because of the word “organic”. I commented.

The Fed may do a brief period of “organic” expansion (which by the way can mean anything the Fed wants), but I propose more QE is coming whether the Fed “intends” to do so or not.

Fed’s 2019 Interest Rate Expectations vs Market’s Expectations

Here’s a look at the Fed’s 2019 Interest Rate Expectations vs Market’s Expectations

I propose the Fed is wrong, again, as usual.

For discussion of today’s FOMC decision, please see Fed Cuts Rates 1/4 Percent, Three Dissents: Dot Plot Suggests No More 2019 Cuts

Dot Plot September 26, 2018

That’s quite a hoot isn’t it?

Even without Covid-19, the Fed was not remotely close to its expectations.

My Dot Plot comment at the time: “I side with those who expect more rate cuts.”

Clueless Wizards

Some people have immense faith in proven clueless wizards. Others think the Fed does nothing but follow market expectations.

However, this creates what would appear at first glance to be a major paradox: If the Fed is simply following market expectations, can the Fed be to blame for the consequences?

More pointedly, why isn’t the market to blame if the Fed is simply following market expectations?This is a very interesting theoretical question.

Fed Uncertainty Principle

I discuss the above paradox in If the Fed Follows the Market, Why Won’t Rates Go Negative?

Corollary number one stands for the for plot example above.

Corollary Number One

The Fed has no idea where interest rates should be. Only a free market does. The Fed will be disingenuous about what it knows (nothing of use) and doesn’t know (much more than it wants to admit), particularly in times of economic stress.

In case you missed the post, please give it a look. There’s lots more in play regarding what the Fed knows and doesn’t.

Message From Gold

Another pair of suspenders is on deck.

Gold has that message. Do you?