The Decade Long Path Ahead To Recovery, Part 2: Depression

Tyler Durden

Wed, 08/12/2020 – 11:00

Authored by Michael Lebowitz and Jack Scott via RealInvestmentAdvice.com,

The first article in this series, Part 1 Debt, details the massive accumulation of debt and how it will handicap economic growth in the future.

Debt is but one crucial economic factor to consider when assessing economic growth. There are three other “D” problems worth considering- Depression, Demographics, and De-globalization.

To assess where the economy is going, you first must know where it is. With that in mind, the focus of this article is depression.

Visualizing a Depression

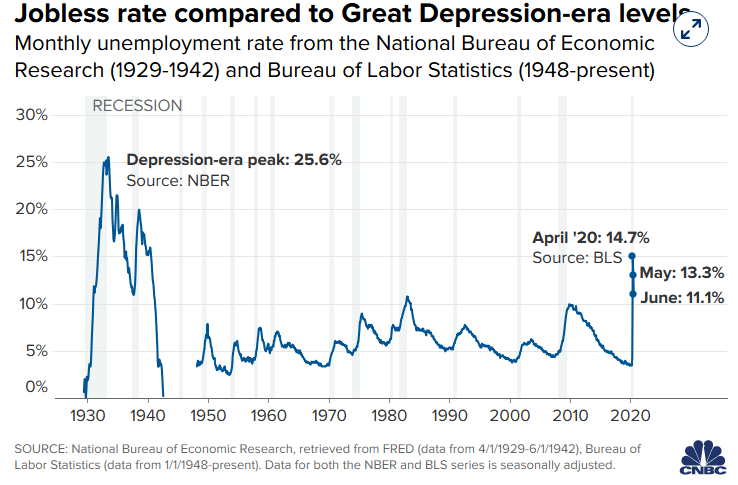

Will the current economic slump be called a recession or depression? No one knows for sure because there is no precise definition of depression. That said, recessions tend to be relatively brief periods of economic contraction – 18 months or less. Depressions, like that experienced in the 1930s, extend much longer. What we do know now is that recent economic data is unlike anything seen since the Great Depression.

Fortunately, the economy appears to be stabilizing and showing signs of recovery. We caveat the statement as recovery rests solely on the crutches of unprecedented Federal and Monetary stimulus. Fed and government actions are not only buying economic growth but time.

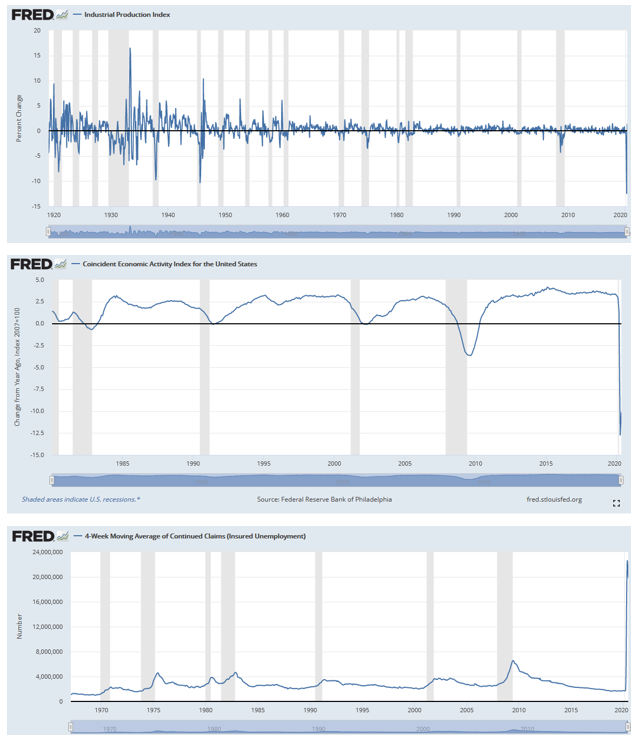

The graphs below show that some of the economic damage seen thus far is mind-boggling.

Uncle Sam to the Rescue

The graphs above could be a lot worse.

The government, with the Fed’s backing, softened the economic blow with a myriad of stimulus programs. For starters, consider $1,200 checks, allowances for the forbearance of mortgages, and generous unemployment benefits. These and other programs allow people to remain solvent and, importantly, to continue spending. They also buy time, hoping that many people and businesses can get back on steady ground.

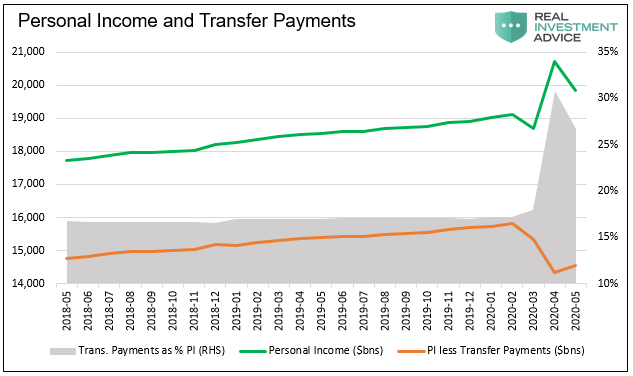

The best way to show how the government indirectly bought economic activity is via personal income and transfer payments. Transfer payments are government checks to citizens. As shown below, personal income plummeted, but personal income, including transfer payments, rose sharply.

Not only did the government make up for lost income, but in aggregate, citizens got a big bonus check. Without over $2 trillion in extra income from the government, annualized real GDP would be 10% lower.

The following graphs offer more context to an unprecedented amount of federal assistance. How will we pay for it given that tax receipts are falling? Ah, that is altogether another question.

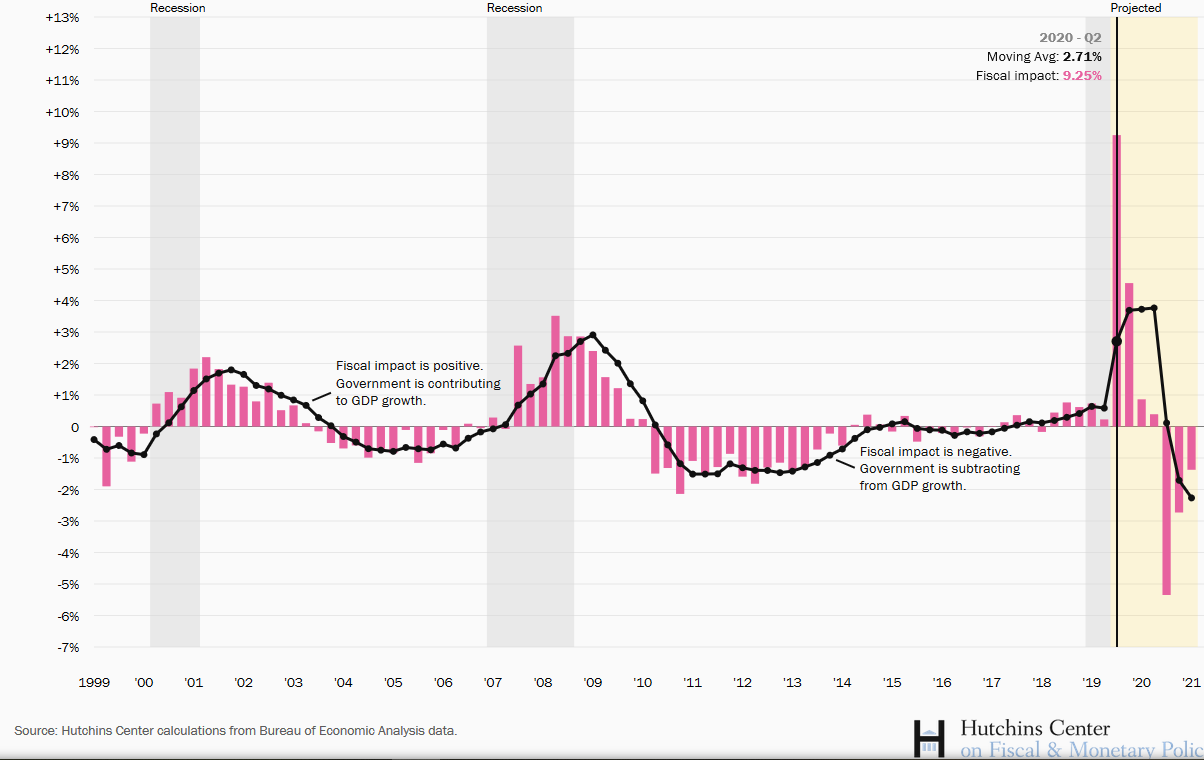

The Hutchins Center provides valuable analysis on the impact of government stimulus on GDP. Per their report, Federal and state stimulus will contribute 9.25% to second-quarter GDP. They expect that amount to fall considerably to 4.55% in the third quarter and .86% in the fourth quarter. By the second quarter in 2021, they forecast an economic drag of 5.35%.

The $1,200 checks have primarily been spent. $600 of additional Unemployment insurance just ended but will likely be extended. Funds borrowed via PPP to pay employees are waning. Time is ticking unless stimulus continues at a breakneck pace.

Consumers

As many as 75% of American workers live paycheck to paycheck. In many of these cases, government programs were a lifeline for the last few months. It bought them time and breathing room. In many cases, they may have lost their job but were financially better off.

For many low to moderate income classes, the stimulus will bridge the gap to recovery. For others, it is a bridge to nowhere with more financial difficulties yet to come.

Now consider more fortunate households with some savings. For those with jobs and savings, the stimulus was mainly a bonus check. In some instances, it was spent, and others saved it or used it to pay down debt. Despite having savings, some in this camp have had their hours reduced or lost their jobs. While savings help, will the stimulus provide a long enough bridge?

Except for the very well-to-do, a majority of the population will emerge from the last few months with a new outlook on spending and savings. It is hard to see how citizens will not refocus on padding their nest eggs. Given the large baby boomer population just entering retirement, this is a big deal.

Consumers drive almost 70% of economic growth, and if savings become a higher priority, the outlook for spending must decline. Prolonged economic weakness, high unemployment, less consumption, and higher savings rates will weigh on the economy for years to come.

Corporations

It’s not just consumers facing headwinds. The following brand name companies have already filed for bankruptcy: Gold’s Gym, J.C. Penny, J. Crew, Modells Sporting Goods, Neiman Marcus, GNC, Chuck E Cheese’s, Lord & Taylors, and many lesser-known entities. There are many others on the brink of bankruptcy that are sacrificing future growth to stay alive.

Most big companies will avoid bankruptcy but will need to retrench to preserve liquidity and profits when possible. Many companies will reduce payrolls, which in turn results in a circular loop as the newly unemployed spend less. Companies are also making less capital and human resource investments to support future probability. The combination will no doubt reduce economic activity.

Companies are raising money at a record pace for liquidity purposes, not for productive investment. The new funds will help bridge the economic chasm, but as discussed in Part 1, at the cost of future growth. Before this year, corporate debt was at record levels to GDP. While only halfway done with the year, corporations have matched debt issuance totals of the prior few years.

In Part 1, we showed how increased government debt will inhibit economic growth. For the same reasons, corporations will contribute less to economic growth.

Municipalities

The following article from Bloomberg, Tax-Averse Nashville Goes Where Few other Cash-Poor Cities Dare, discusses the impact that COVID is having on Nashville’s finances and the tough decisions it is making.

While the article is about the city of Nashville, it rings true for many states, counties, and cities throughout the United States. From the article:

“Congress has earmarked $150 billion for states and local governments — Nashville is slated to receive $122 million but the money must be spent on public health and can’t be used to fill budget holes.

State and local governments are in “uncharted territory” and will have to start making serious cuts if they don’t get more help, said Richard Auxier, a senior policy associate in the Urban-Brookings Tax Policy Center.”

Unless the government draws up a second and third round of muni bailouts, many state and local governments will have no choice but to raise taxes, lay off employees, and reduce services.

Like the Federal government, corporations, and citizens, municipalities will contribute less to economic activity. They, too, will be a drag on economic growth for some time to come.

Summary

Like a pack of cigarettes, the economy of the 2020s should come with a boldly labeled warning: The economy may be hazardous to your wealth.

Despite many indicators that economic growth, and therefore corporate profits, will grow meagerly, markets are priced for a renewal of prior growth rates. We caution, in the long run, reality always trumps hope.

While the government may keep spending like a drunken sailor, the other sectors of the economy will have no choice but to hunker down. Government spending comes at a cost in the future, as we discussed in Part 1. The effects of the rest of the economy are likely to hit much sooner.

The bottom line- the recession or depression will have a lasting and negative effect on growth for years to come.