Saxo: “Trump’s Address To The Nation Failed Abysmally In Calming Sentiment”

Submitted by Eleanor Creagh of Saxobank

Summary: The resounding theme throughout markets is too little too late when it comes to policymakers promises. With fiscal stimulus measures likely to fall short of what is required, monetary stimulus ineffective in the virus fight, and public health policy seriously lacking when it comes to preventative measures and availability of testing destroying confidence. We await the ECB tonight, will Lagardes bazooka be enough

* * *

President Trump’s address to the nation failed abysmally in calming sentiment, with the speech driving a risk assets into the abyss. US futures plunging – Nasdaq futures trigger limit down at 7,590, Asian indices all firmly in the red and European futures pummelled. Overnight Index Swaps pricing an immediate emergency cut tonight by the Fed. Both Brent and WTI futures crashed more than 6% and Euro Stoxx futures more than 8% at one stage as President Trump implements a ban on all travel between the US and Europe (excludes UK) for 30 days beginning Friday local time.

It seems we underestimated yesterday in saying, in this heightened volatility regime 3% days, both to the upside and downside, will be the new normal. Todays 7+% plunge on the Aussie market begs to differ! Australian stocks sinking deeper into a bear market with today’s trade dictated by the lacking US rescue package that sent US futures tumbling. We still maintain that to have real confidence in buying into any relief rally volatility needs to reset meaningfully lower. And more clarity surrounding both the economic consequences of measures to control the spread of COVID-19 as well as the stimulus hopes is needed. It is too early to tell whether the health crisis will develop into a more serious global financial/credit crisis or how deep and dark a recession would be. Confidence is frail and the fear of the unknown and prospect of aggressive economic shutdowns is enough to keep risk assets under pressure. As we said yesterday, there will come a time for bargain hunting, but we are inclined to wait it out.

As well as the travel ban which really shook risk assets, President Trump’s speech detailed:

- Financial relief for workers “who are ill, quarantined or caring for others”

- Plans to defer tax payments for some individuals and businesses for up to three months

- Plans to make low-interest loans available to businesses

- A call to Congress to pass a cut to the federal payroll tax

But what markets really want here is less talk and more action. The administration will need to provide more details and concrete measures quickly in order to inject an air of calm into risk assets, if only temporarily. However, a key issue remains, what you don’t know, you cannot quantify – public health measures need to lead the charge with widespread testing/preventative measures to provide more confidence in containment measures and in the case count data. How can we discount a recession or recession in corporate earnings without knowing the scale of the health crisis or true impact. And how can communities overcome widespread panic without knowing what they are up against.

Whilst there is so much uncertainty in the case count and spread of the virus and consequently the virus fight, there can be little consensus or confidence in appropriate policy responses. Although stimulus packages may ease downside risks to the economy, for markets and community sentiment to really recover the onus will be on reduced COVID-19 transmission rates, increased immunity and a clear containment of the outbreak.

Australian Government Package – Finally the fiscal as well as the monetary lever has been pulled

At long last the surplus obsession has been put aside and the government are working in a coordination with the RBA to provide relief for the struggling economy.

- The gross impact of the stimulus package is A$22.9bn over this financial year and the next 2, 1.2% of GDP. As a percentage of GDP this is a similar sized package to the initial measures provided by the Kevin Rudd government in 2009.

- Stimulus payments to households: Payments of A$750 to pensioners and other income support recipients

- Support for business investment: A$700 million to increase the instant asset write off threshold. Businesses with a turnover of up to A$500mn will now be able to write off purchases of up to A$150,000.

- Cash flow assistance for businesses: A$6.7bn over 4 years will be spent on helping small businesses affected by COVID-19 maintain operations and pay wages throughout this period of economic dislocation. Up to 120,000 apprentices will also be getting support payments to keep them employed and 650,000 small and medium-sized employers will have access to grants of up to A$25,000

- Assistance for severely-affected regions: $1bn to support those most affected by the economic impacts of COVID-19, centred on tourism, agriculture, China exposed exporters and education. Tourism is one of the hardest hit industries in Australia via the slowdown in Chinese visitors at present, but with new travel bans being enforced across the globe every 24h the worst is yet to come. We are yet to see if Australia will follow suit with a travel ban from Europe may be implemented following President Trump’s announcement this morning.

Total immediate payments are worth about A$11bn and will be expedited by the government to be delivered by the end of June. The frontloading is aimed at avoiding economic contraction in the June quarter that would see a technical recession recorded in Australia. However, the June quarter will still be subject to much uncertainty given that entering into the colder season the COVID-19 virus could be inflicting severe consequences locally. If the virus spreads domestically in the colder season border closures, shutdowns, cancelled events, quarantines and social distancing measures will present a further shock to economic activity.

A Good Start

The package is certainly a welcome development and a good starting point, but don’t forget the Australian economy comes from a position of weakness and desperately needed the fiscal contribution PRE virus. The economy has lost momentum since the 2nd half of 2018, unemployment has risen, the private sector is in recession and both business and consumer confidence has been mired. Again all PRE virus. And more recently the bushfires and drought have also served a 1-2 punch to Australia’s economy. The COVID-19 outbreak continues to spread globally and as transmission increases, so does fear and preventative measures become more drastic and disruptive to the global economy. This is likely just the first line of defence when it comes to fiscal stimulus for the Australian economy.

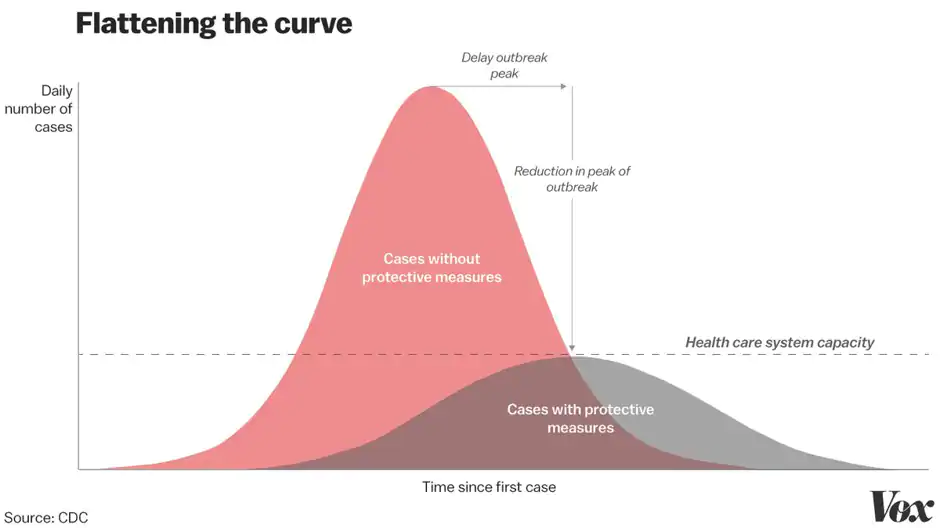

Why is the containment so important? the speed at which the outbreak plays out matters hugely for its consequences. Preventing a large spike in cases via social distancing, quarantines and border closures is key to preventing the health care system becoming overwhelmed by surging cases. In that scenario, the mortality of the disease rises because there hospital beds are overloaded, staff are spread too thin and there is not enough medical equipment to deal with the case load.

In many countries, such as Australia, the outbreak is only in its infancy and evolving rapidly making it very difficult to gauge the scale and true impact of this health crisis. As such it is not possible to quantify what will be needed in terms of stimulus measures, but the longer it takes to contain the COVID-19 outbreak the more support economies will need as both supply and demand is hit.

Focus on SMEs and Jobs

The focus on business and jobs is the correct approach as opposed to targeting households who would have a higher propensity to save the payments.

“This plan is about keeping Australians in jobs,”

Besides the hit to demand and supply, the a key area of concern for Australia is the labour market given the level of household debt. This is why the stimulus package is focussed on allowing businesses to prevent layoffs and supporting “business as usual” so as to limit potential knock on effects. Australia has a very high level of household debt relative to other OECD countries, with household leverage ratios at almost 2x incomes. This means that whilst people are employed debt is serviceable, but if unemployment were to become a significant issue that debt might not be so serviceable and could prompt a more serious economic fallout. That is why it is paramount for the government and the RBA to consider maintaining job security as focal point in any stimulus response. One area where the Morrison government has the right focus, stating

Business focus, “because our goal is to keep people in work”

The package will boost cash flow for SMEs to enable those under pressure to pay wages, invest and most importantly prepare for the downturn. Whilst we doubt too many businesses will be employing more staff, the cash flow support will be vital in providing goodwill payments to casual workers who lose shifts, extended sick pay for those unable to work and preventing layoffs for those businesses facing a material impact from the COVID-19 outbreak. The focus on small business via the changes to the instant asset write-off scheme and cashflow assistance is a key measure. Although with confidence already mired investment may not receive the boost it could have in more certain times. However this will be countered by the fact that the write of will only last until June and therefore there is an motivation for businesses to utilise and the boost to the economy will be timely. Many small businesses on average only have about three months of cash-flow to withstand shock. Therefore, preventing SME cashflows from drying up via the cashflow assistance whilst revenues and operating incomes are scourged by the simultaneous demand and supply hit will be a vital lifeline in halting a more broad based shock and preventing staff layoffs.

Cash handouts will be relatively ineffective in boosting household spending during this protracted period of economic uncertainty. By targeting those already receiving benefit payments, the propensity to spend quickly rather than save, providing a timely boost to the economy will be increased. It will provide relief for those really suffering but is not enough to encourage any meaningful consumption boost for the economy, particularly whilst the health crisis rages globally. As we saw last year with the Morrison government’s tax refunds, the propensity to the save the cash handout was increased and whilst a global pandemic is looming that would once more be the case. We only have to look to the pandemonium that has erupted in supermarkets as consumers panic buy essentials to see the level of fear in many communities.

In yesterday’s Westpac consumer confidence release the unemployment expectations subindex rose more than 11 points. This measure is heavily influenced by survey respondents real world experiences and is typically influenced by friends/family experiences so is a leading indicator of unemployment. Whilst this sort of fear and uncertainty prevails consumer spending will be materially weaker with or without cash handout, a problem given consumption is 60% of the economy.

A major problem here is the hit to sentiment and therefore demand cannot easily be reversed by monetary or fiscal policy. Whilst consumers are fearful of the threat of a global pandemic, confidence will be hard to restore, hence why containment efforts are so important in supporting confidence.

To boost confidence public health policy needs to lead the charge along with the fiscal policy measures that ease uncertainties surrounding job security and support businesses to prevent layoffs. Widespread testing has not been available in most developed countries and whilst this is lacking the fear of the unknown reigns, and people cannot accurately quantify how big this crisis really is. This represents a failure of most governments and health officials that leads to a serious erosion of confidence beyond the economic ramifications.

Tyler Durden

Thu, 03/12/2020 – 08:14