Here Are All The ETFs That Will Be Bought By The Federal Reserve

Now that the Fed has effectively nationalized the bond market (don’t worry, stocks are next, it’s just a matter of time) which all the way down through junk bond issues and CLO tranches will no longer reflect the underlying fundamentals but merely what mood the Fed is in on any given day, and where it it tells Blackrock to close the market, the only thing that matters for traders is how to frontrun the Fed, so to make sure that the Fed’s helicopter paradrop is utilized by everyone in the most efficient way, here is a breakdown of everything the Fed will be buying to make sure the bond prices of fallen angels – firms which spent trillions on stock buybacks instead of even considering a downside case – trade near par even as the underlying cash flows drop near zero.

But first some background: the Fed’s revised, and massively expanded, Secondary Market Corporate Credit Facility – which now can purchase ‘fallen angel’ junk bonds – will now be funded with $25 billion of equity capital from the Treasury as opposed to $10 billion previously. The leverage on the equity will be 10x for IG-rated bonds, 7x for bonds below IG, and in a range of 3x to 7x for any other eligible asset. The scope of the facility was also expanded, and in what was the biggest news of Thursday, while it was originally targeted toward IG bonds from US issuers and US-listed IG ETFs, the facility can now also purchase:

- BB-rated bonds of recent “fallen angels” so long as they were IG rated as of March 22, 2020, and

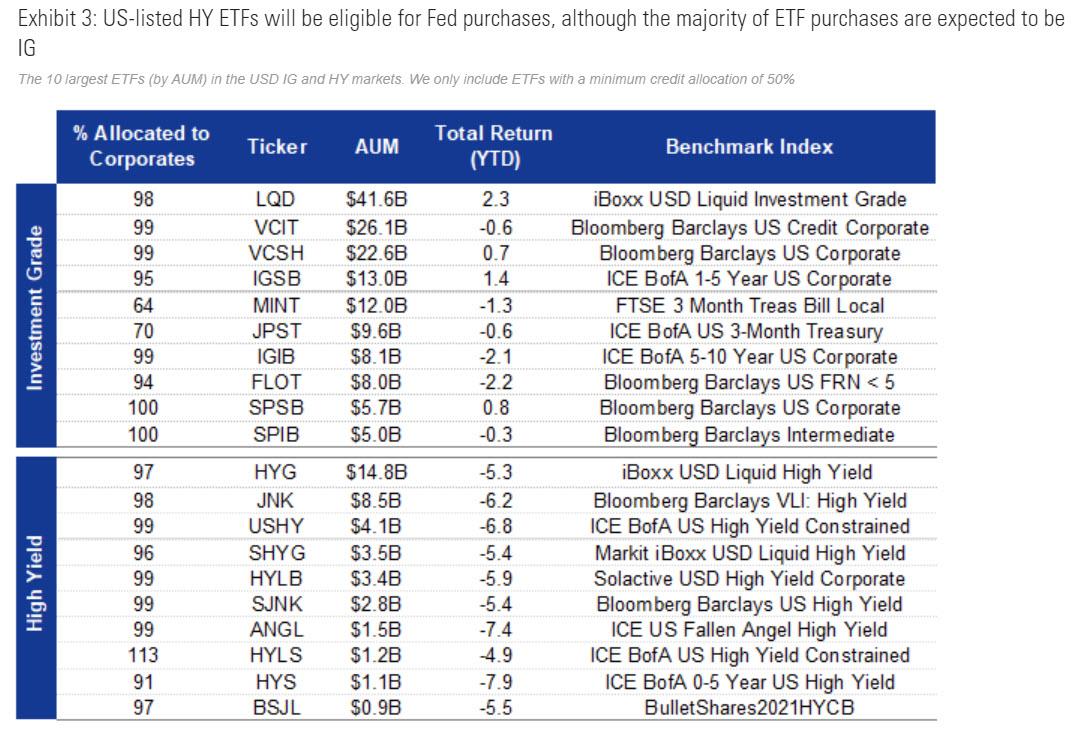

- HY ETFs, although the “preponderance” of ETF holdings are expected to be IG.

Additionally, as Goldman notes, while the limits for bond and ETF purchases remain the same (10% of an issuer’s outstanding debt and 20% of ETF assets, respectively), a new comprehensive issuer limit was added: 1.5% of the combined potential size of the Primary and Secondary market facilities (which will be $750 billion, per the above), equating to $11.25 billion. The details on issuer eligibility were also expanded to include being “created or organized” in the United States and having the “majority” of employees based in the United States, which means that many foreign companies will find their bonds purchased under the Fed’s “loopholes.” Finally, the updated language also makes it clear that Banks are explicitly excluded, in addition to sectors receiving direct government support as part of the CARES Act.

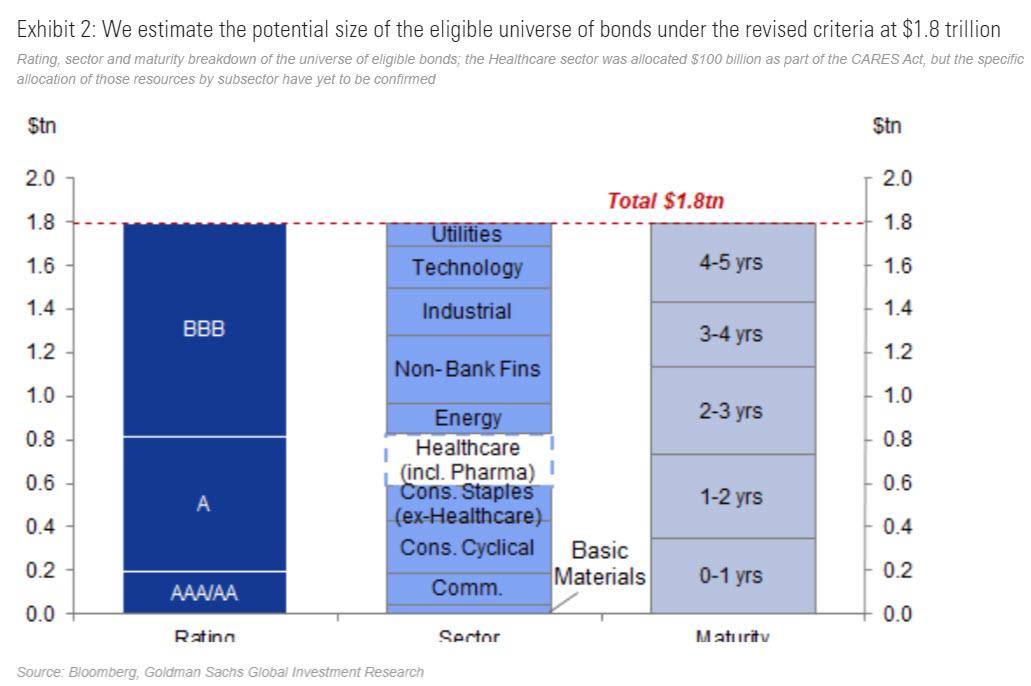

Putting this together, Goldman estimates that the potential size of the eligible universe of bonds under the revised criteria at $1.8 trillion.

And here is the answer to everyone’s question: with the Fed not yet buying stocks, what is the next best thing to buy in frontrunning the Fed that carries the highest possible return, and the answer of course is junk bond ETFs.

So after accounting for the above limits per issuers, the effective ceiling on purchases within the $1.8 trillion is $450 billion, in face value. For ETFs that have at least a 50% allocation to credit, the total assets under management before applying the 20% limit is $194 billion and $47 billion in IG and HY, respectively. The full list of US-listed investment grade and HY/junk bond ETFs that are eligible for Fed purchases, and which will almost certainly outperform non-Fed backstopped assets, is the following.

Looking at the list above, anything that has a negative total return YTD will put a frown on the Fed’s face, and only disproportional buying of said ETFs – with complete disregard for the underlying fundamentals because there is a reason why these ETFs, mostly consisting of junk bonds issued by private equity portfolio companies operating in the energy sector, got hammered in the first place – will turn the Fed’s frown upside down.

Which begs the question: when will the industrious financial wizards at Blackrock, who incidentally are so conflicted they are executing the Fed’s purchases, put together an ETF consisting only of ETFs that are now purchased by the Fed? Because something tells us that particular ETF would do phenomenally well in the coming months as the US economy slides into a depression.

Tyler Durden

Fri, 04/10/2020 – 15:50