Why A New Diplomatic Crisis With China Is Critical For Trump If He Wants To Be Re-elected

Amid all the discussion of whether (or not) it is time to reopen the economy, and take the potential risk of a second wave of infections and deaths resulting in what could be a far more devastating second shutdown, one overlooked angle on the Corona-lockdowns as pointed out by Nordea’s FX strategist Andreas Steno Larsen, is that it emphasizes the already growing barriers between the “Elite” and the “Workers.”

In his latest FX weekly observations, Larsen writes that while “the big cities are the main epicenters (also per capita) of the Covid-19 virus, containment measures have been forced upon entire states and countries.” As a result, regions with low density have been faced with the same kind of measures as more dense areas, even if these regions haven’t seen a material spread of the virus.

In other words, “One size fits all, even if density has proven to be maybe the biggest issue when trying to contain the virus spread.” This means that in addition to the outsized gains to the elite as a result of the trillions in new stimulus injections which have promptly buoyed capital markets, the current virolocracy could also be seen as “both extraordinary elitist and gentrification-supportive in its nature, since a much larger part of the urban population can work from home etc.”

Expanding on this argument, Larsen notes that “workers lives matters” has seen tailwind in important swing states such as Michigan as most of the spread has been seen around Detroit, while the less dense parts of the state haven’t seen any material spread of the virus. The movement argues that the big cities are relatively better off in the lockdowns, and that less dense areas should never have been forced to close the economy anyway. And as the Nordea strategist writes, “it is KEY for The Donald to win over such “movements” if he wants to triumph in the election later this year.”

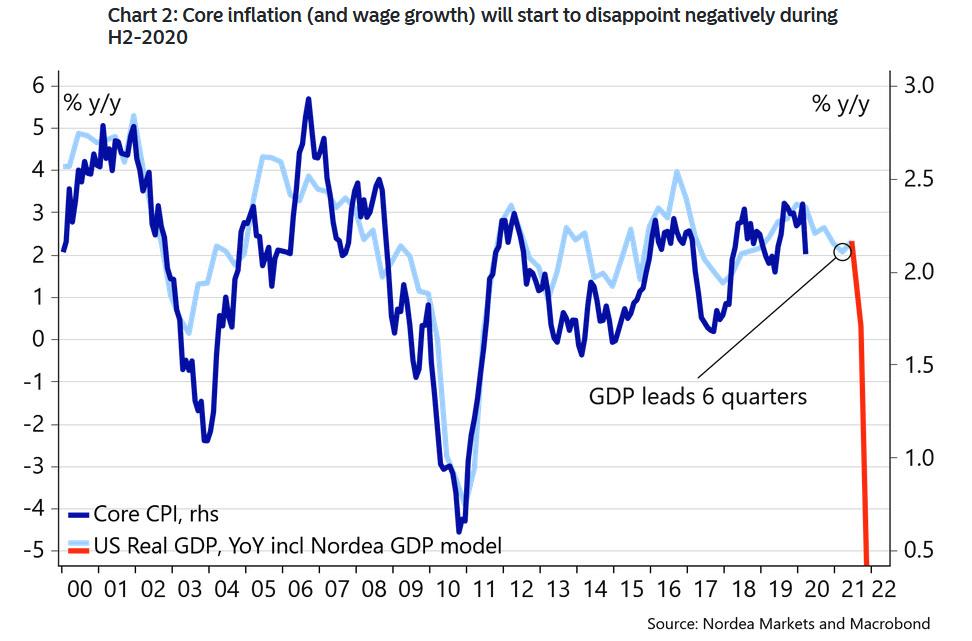

The problem is that neither Nordea, nor the Fed, think the economy will be in a good shape by then, which is why The Donald needs something else to convince his base, in particular since wage growth could be about to fall of a cliff.

Indeed, wages are another reason why workers are about to get a double whammy of corona pain: as Larsen continues, core inflation (and wage growth) are cyclical laggards, which means that first

- activity comes to a halt,

- commodity prices and headline inflation drop,

- workers are laid off in size,

- wages and prices decelerate or even decline.

Nordea believes that we are probably in between phase three and four now, and why news on prices and wages will be the next to surprise negatively during H2-2020 and in to 2021 (in Q1 and Q2 activity data has been the negative surprise).

So faced with record unemployment coupled with growing labor class anger, Trump’s weapon of choice to win over the workers again, will be an escalation of his China-bashing strategy in combination with renewed isolationism.

According to Nordea Trump deeming Chinese equities a “national security risk” is not really newsworthy since the EU has been talking about the same thing for a while – though, mostly with a focus on blocking potential hostile Chinese take-overs of Euro area companies, but it suddenly seemed to revive the focus on geopolitical risks on the other side of the Corona mess.

And while the US/China trade deal has been stone-dead for months already (as it was from the outset), so that is in itself not exciting, no-one had an interest in saying so until after the US election. The corona virus – and the coming elections – have offered Trump a chance to “reveal” that the trade deal is 100% off, and to take a renewed China aggressive stance into the election instead.

This inevitable deterioration in diplomatic relations, as Larsen concludes, is bad for Asian FX (versus USD), and risk assets and equities in general, and why Rabobank earlier today said that “There Is One Key Thing To Watch Today: The Yuan.“

As Larsen concludes, “Before the March melt-up in markets, USD/CNY was THE global bellwether for risk appetite, and it may very well return as such very soon. You should buy USD/CNY (and sell risk assets) on tariff threats.”

Tyler Durden

Mon, 05/04/2020 – 20:10