US Oil Rig Count Crashes To 11-Year Lows: “There’s A Double Risk On The Horizon”

Tyler Durden

Fri, 05/15/2020 – 13:09

Well that escalated quickly…

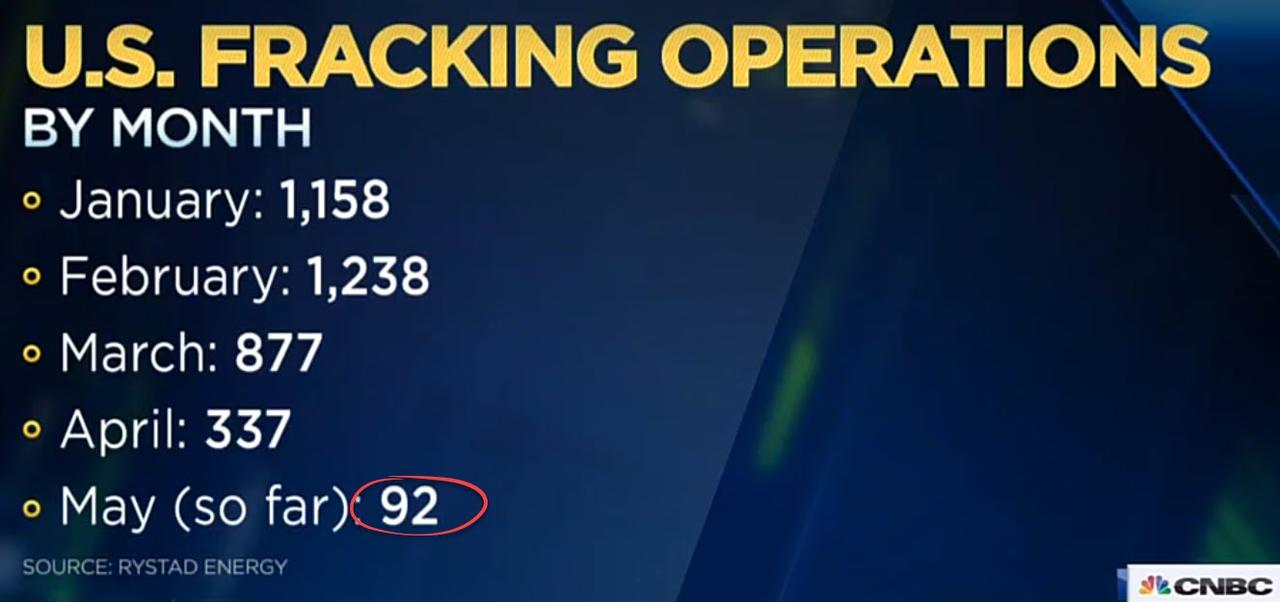

Drilling rigs targeting crude oil in the U.S. fell by 34 to 258, the lowest since July 2009… and production is starting to collapse…

Source: Bloomberg

Indeed, as OilPrice.com’s Hely Zaremba notes, US Shale needs to slow down to survive…

Rigs targeting oil in the:

-

Permian: -23 to 175

-

Eagle Ford: -3 to 23

-

DJ Niobrara: unchanged at 7

-

Williston: -4 to 16

-

Cana Woodford: unchanged at 4

-

Others: -2 to 29

It has been a bleak couple of months for oil markets. Although markets recovered after going negative for the first time in history earlier this month, they didn’t recover to nearly their pre-corona levels, and all of the factors that pushed the West Texas Intermediate crude benchmark to nearly $40 below zero per barrel still persist. Thanks to a pandemic-fuelled oil price war between Saudi Arabia and Russia, the leading OPEC+ members, there continues to be a massive global oil glut and a worsening storage deficit. Things have been looking up, however. The output cuts have made a dent in the global oversupply and demand is beginning to recover a bit after taking a huge hit from industrial shutdown due to the pandemic.

On Monday Saudi Arabia announced that it will impose even more production cuts, and markets rose in response.

“Saudi Aramco, the state-controlled oil company, will produce 7.5 million barrels a day in June, down from more than 12 million in April,” reported Barron’s. Although Saudi Arabia has been overtaken by the United States as the biggest oil producer in the world thanks to the latter nation’s “shale revolution,” Saudi Aramco’s decisions are still hugely influential on the global stage.

Their production cuts therefore bode extremely well for the international oil markets.

But it’s not all sunshine and roses.

“There’s a double risk on the horizon,” writes Julian Lee in an opinion piece for Bloomberg.

“Just as lifting lockdowns too soon could bring a second spike in virus infections and deaths, loosening the hard-fought restraint in oil production too soon risks a second oil-price collapse.”

The United States will have to walk a very fine line if they want to have any chance at reviving the shale industry that is currently drowning in a wave of bankruptcies and fired and furloughed employees.

As restrictions are being eased in many countries around the world, oil demand is beginning to pick up, but “it is still far from the year-on-year growth we experienced before the novel coronavirus struck, or from any kind of meaningful start at drawing down ballooning stockpiles. But it might just be an initial turning of a corner — as long as there’s no need to stop the global economy again to keep the Covid-19 outbreak under control,” opines Bloomberg’s Lee. The opinion column looks to the way that China, which is ahead of the rest of the world in its pandemic curve, for how they have navigated the delicate balance between opening up the economy and preventing a COVID-19 resurgence.

The situation in China can teach us a lot about what to expect for fuel demand in the coming months.

“Congestion on roads in major cities has soared during peak commuting hours, but it remains depressed outside those times, with traffic levels still well below normal during the weekend and on holidays,” writes Lee.

“Meanwhile, people are choosing to drive rather than take public transport, boosting gasoline demand, a trend that’s likely to continue for a considerable time in big cities around the world. In Beijing, for example, subway passenger numbers are still more than 50% below pre-virus levels, according to analysis by Bloomberg NEF.”

It will be tempting, in the United States, to see a light at the end of the tunnel and open the shale fields back up in an effort to revitalize the economy, but this would be premature and short-sighted. The positive effects of reductions in oil production are just now starting to kick in and need to be prolonged.

“But we are still a long way from seeing much relief for crude producers and they need to continue exercising restraint,” says Lee. “The real risk may be that when all the financial pain of output cuts — and the human cost of job losses — starts to pay off with higher oil prices, producers take it as a signal to restart the pumps, as if the whole oversupply problem got solved overnight. The output restraint has to last long enough not only for supply and demand to be brought back into line, but for stockpiles to be brought back down again.”

What’s more, the United States is not Saudi Arabia. Without the authoritarian power that many petro-nations have, the decentralized, privatized leadership in the U.S. the oil industry means that the country can’t stop and start pumping on a dime.

This means that the U.S. has to be extra cautious about making any serious changes to current oil production patterns because the ship can be slow and difficult to right.